Setting up a holding company in Andorra: tax advantages and organizing your assets

Introduction

Setting up a holding company in Andorra is never a simple technical matter.

It is a structural decision that affects governance, cash flow, legal certainty, and, very often, the ability to organize assets over the long term.

Andorra's appeal is real: a stable institutional framework, modern corporate law, and competitive taxation.

But this attractiveness is too often presented as a ready-made, almost automatic solution.

However, an Andorran holding company is neither universal nor magical.

Its relevance depends on the objectives pursued, the nature of the assets, the profile of the decision-makers, and the international environment in which the structure operates, in a context of increased fiscal transparency.

This article makes a clear promise: to provide you with a strategic, asset-based, and tax-related framework for assessing, with discernment, whether a holding company in Andorra is relevant, sustainable, and defensible in your situation.

As a bonus, this article gives you access to a comparative tax simulator, designed as educational and decision-making tools, allowing you to compare the effects of structuring via a holding company in Andorra with other jurisdictions such as France, Spain, the United Kingdom, Germany, and other countries, as applicable.

If you want to go further, the full article, which also includes the simulator, is available to save you time and quickly visualize the key points.

If you are considering setting up a holding company in Andorra or reevaluating an existing structure, ENGAGE can assist you with a structured and confidential analysis to align your wealth and business organization with your real and long-term goals.

Finally, to make reading easier, you can approach the text as a guide à la carte, based on the outline provided.

I. What is a holding company (and what it is not)

I.1. The economic function of a holding company

A holding company is a company whose main purpose is to hold shares in one or more other companies.

It is located upstream of the operational entities and performs a holding and steering function, without intervening directly in day-to-day economic activity.

Through this function, the holding company primarily enables the centralization of control over several companies within a single structure.

This centralization facilitates strategic decision-making and provides a consolidated view of all the group's activities.

The holding company also makes it possible to organize the governance of a group in a more transparent and consistent manner.

It constitutes an intermediate level where general guidelines, management rules, and internal control mechanisms can be defined.

Financially, the holding company plays a central role in structuring economic flows.

It enables the organization of dividend payments, cash management, financing of subsidiaries, and the reallocation of resources to new investments.

This financial function contributes to better control of the group's financial balance and a more rational allocation of capital.

Finally, the holding company offers the possibility of separating the risks associated with operational activities from the overall assets.

By isolating certain functions or assets at the holding company level, it becomes possible to limit the legal and financial exposure of the partners.

This results in a more secure structure, both for day-to-day operations and for asset ownership.

However, it should be noted that holding companies are not a business in themselves.

It creates value only through the function it performs and the way it fits into the overall organization.

Its relevance therefore depends on its consistent integration within the group's legal, economic, and asset structure.

It is in this overall structure, and not in the formal existence of the holding company, that its true usefulness lies.

I.2. The main types of holding companies

There are several different types of holding companies, each with significantly different purposes, operating methods, and legal implications.

These distinctions are not purely theoretical.

They determine the structure of the group, the degree of involvement of the holding company, and the analysis of its economic substance.

A pure holding company is limited to holding shares in other companies and exercising the rights attached to shareholder status.

Its role is essentially passive, focused on holding capital and potentially collecting income.

It does not intervene in the operational management of subsidiaries and does not assume any management or coordination functions.

This type of holding company may be appropriate for asset management, long-term ownership, or simple capital organization purposes.

However, it requires particular vigilance in terms of substance and economic justification, particularly when the structure is established in a specific tax environment.

The absence of specific activity must then be compensated for by clearly identifiable overall consistency.

The holding company stands out for its active role within the group.

It participates in defining the overall strategy, coordinating subsidiaries, and providing internal services such as administrative, financial, and management services.

This leadership role requires demonstrable operational reality, both on a human and organizational level.

In return, it strengthens the economic coherence of the group and allows for a more substantial reading of the structure.

It can also facilitate certain structuring operations, provided that its role is real, documented, and sustainable.

The asset or family holding company follows a different logic.

It is mainly used to organize the holding of assets, whether these are shareholdings, real estate assets, or financial investments.

Its objective is part of a broader vision of heritage protection, transmission, and family governance.

In this context, the holding company becomes a long-term tool, designed to support the stability of holdings and intergenerational continuity.

It allows you to anticipate family changes, organize powers of attorney, and structure decision-making rules within a secure framework.

The choice of holding company structure cannot therefore be separated from the objectives pursued and the overall context in which the structure operates.

It is this alignment between the chosen form and the desired outcome that determines the relevance and soundness of the proposed structure.

I.3. What the holding company does not allow

It is essential to remember what a holding company does not do, in order to avoid any simplistic or overly optimistic approach to this type of structure.

A holding company, regardless of its location, does not in itself alter the fundamental principles of international tax law.

It does not remove the tax rules applicable in the states where the income is actually generated.

Profits remain subject to local laws, tax treaties, and withholding tax mechanisms specific to each jurisdiction.

Nor does it exempt one from demonstrating the existence of a real economic substance.

The existence of a holding company requires proof of effective resources, functions, and decisions consistent with the role assigned to it.

It does not, on its own, neutralize the risks of reclassification or double taxation.

In the absence of rigorous structuring and in-depth analysis of cash flows, tax authorities may challenge artificial or insufficiently substantiated arrangements.

Nor is it a substitute for a comprehensive analysis of the tax residence of executives and shareholders.

Personal circumstances, places of effective management, and economic interests remain decisive factors, regardless of the existence of a holding company.

The holding company must therefore be viewed for what it really is.

It is a legal and organizational instrument, not an end in itself.

Used without a clear strategy, overall consistency, or risk anticipation, it can become a source of complexity and insecurity.

Under these circumstances, far from being a leverfor optimization, it may expose its beneficiaries to additional constraints and costly challenges.

Conversely, when integrated into a structured and controlled approach, a holding company can make a useful contribution to the organization and security of a wealth management or entrepreneurial project.

II. Why Andorra: legal, economic, and tax considerations

II.1. Andorra's position within the European environment

Andorra occupies a unique place in the European landscape.

A small sovereign state, over the years it has developed a modern legal framework and a structured tax system designed to support economic development while ensuring legal certainty for stakeholders.

For several years now, the Principality has been undergoing a profound transformation of its regulatory environment.

This development has resulted in a gradual and deliberate alignment with international standards on transparency, information exchange, and tax cooperation.

This fundamental shift is by no means insignificant.

It involved overhauling numerous practices, adapting institutions, and increasingly integrating Andorra into international compliance mechanisms.

This permanently changed the perception of Andorra.

From a jurisdiction once perceived as atypical, sometimes misunderstood or caricatured, it has become a legally transparent and structured environment.

Today, Andorra participates fully in international exchanges and is committed to active cooperation with other tax administrations.

It is subject to compliance requirements comparable to those of its European neighbors, both in terms of economic substance and governance and transparency.

This paradigm shift requires a renewed interpretation of Andorran legal structures.

It calls for moving beyond approaches inherited from the past and viewing Andorra as a modern, integrated, and demanding jurisdiction, where legal and economic consistency is now an essential prerequisite.

II.2. A coherent economic rationale for certain strategies

The use of a holding company in Andorra can serve several distinct purposes, most often as part of an overall strategy for organizing business activities and assets.

This may involve centralizing the holding of international shareholdings in order to have a single, transparent, and legally structured point of control.

This centralization facilitates the management of shareholdings, provides a consolidated view of investments, and facilitates the coordination of strategic decisions.

The Andorran holding company can also be a useful tool for structuring an entrepreneurial group within a stable institutional framework.

It helps organize relationships between different entities, clarify roles, and strengthen consistency across the entire group.

From a wealth management perspective, a holding company can be used to organize family assets with a long-term vision.

It then becomes an instrument of stability, designed to support asset preservation, family governance, and continuity in wealth management decisions.

Finally, the holding company can be used to prepare for a future transfer or sale.

By anticipating these operations, it enables the structuring of assets, the ordering of cash flows, and the securing of key stages in a capital evolution.

However, this consistency cannot be imposed.

It only exists if the structure is designed in close connection with the group's actual activities.

The functions performed by the holding company, the flows it organizes, and the decisions it makes must reflect a tangible economic reality.

It is equally essential to take into account the personal circumstances of executives and shareholders.

Their tax residence, their effective role in management, and their economic interests directly determine the soundness of the chosen structure.

It is in this alignment between objectives, operational reality, and personal circumstances that the holding company in Andorra can find its true relevance.

II.3. Who is Andorra really aimed at?

The Andorran holding company is not suitable for all profiles and does not respond to all situations.

Its relevance depends heavily on the nature of the activities concerned, the time frame envisaged, and the ability to establish a coherent and sustainable structure.

It can be a particularly suitable tool for entrepreneurs with international activities.

In this context, it allows for the centralization of shareholdings located in several jurisdictions and the organization of group management within a stable and legally transparent environment.

The Andorran holding company can also meet the needs of family groups wishing to structure and transfer their assets.

It provides a framework conducive to organizing asset management, establishing governance rules, and anticipating intergenerational issues.

It may also be of interest to investors seeking a stable environment in which to centralize assets.

The holding company then becomes an anchor point for securing investments and planning their development with a long-term perspective.

However, the Andorran holding company is rarely suitable for certain configurations.

It is not well suited to purely domestic structures that lack any international or cross-border dimension.

It is also inappropriate when the main motivation is to achieve short-term tax savings.

Arrangements based solely on opportunistic logic are now particularly vulnerable to being called into question.

Finally, it cannot be a viable solution in situations where economic substance and governance cannot be credibly established.

The lack of real resources, effective functions, or demonstrable decisions weakens the structure and compromises its sustainability.

The Andorran holding company should therefore be considered a demanding tool, reserved for projects that are sufficiently structured to justify its existence and usefulness.

III. The tax advantages of a holding company in Andorra: reality, scope, and conditions

III.1. The general framework for corporate taxation

Andorra has a moderate corporate tax rate, applicable to companies considered residents under Andorran tax law.

This regime is part of a now stable legal framework based on clear rules aligned with international standards.

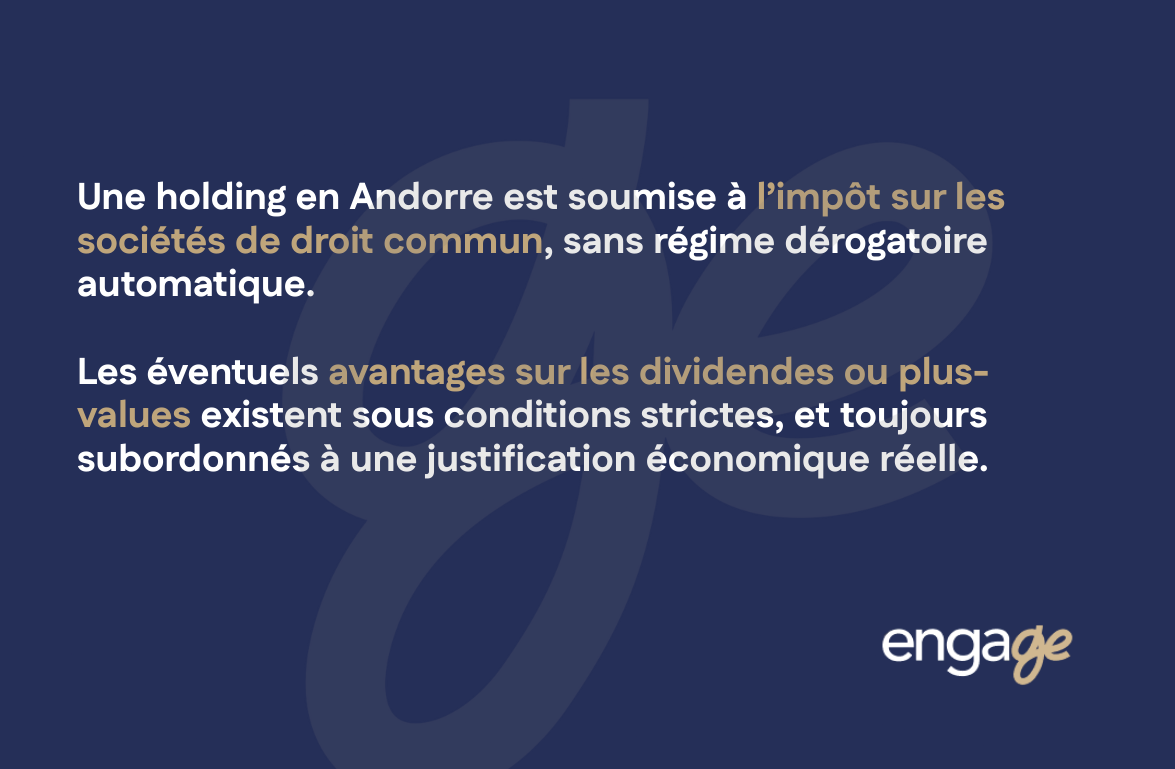

In this context, a holding company established in Andorra is subject to the common rules of corporate income tax.

It does not benefit from an automatic exemption and must comply with all reporting and accounting obligations applicable to resident companies.

However, certain categories of income may be subject to specific regimes provided for by Andorran tax legislation.

This is particularly the case for dividends and capital gains received by a holding company in connection with the holding of equity interests.

Under certain conditions, this income may be eligible for favorable tax treatment.

The application of these regimes requires strict compliance with legal criteria, both in terms of the nature of the shareholdings and the duration of ownership or level of shareholding.

Beyond formal requirements, the tax authorities are placing increasing importance on the economic justification for structuring.

The holding company must be consistent, based on a real organization, and meet identifiable and legitimate objectives.

In the absence of this consistency, the expected benefits may be called into question, regardless of apparent compliance with technical criteria.

The taxation of Andorran holding companies cannot therefore be considered in isolation.

It must be analyzed as one element of a larger whole, incorporating economic substance, effective governance, and the reality of the flows organized by the structure.

III.2. Essential conditions for access to benefits

The potential tax advantages of a holding company in Andorra are never automatic and should not be taken for granted.

They result from a set of cumulative conditions, compliance with which determines the security and sustainability of the structure.

The first pillar is based on the substance of the holding company.

It must have suitable premises, effective governance, and real and demonstrable decision-making mechanisms.

The formal presence of a company is insufficient if it is not accompanied by human, organizational, and decision-making resources consistent with its role.

The second pillar relates to the economic coherence of the structure.

The holding company must be part of an identifiable group structure and perform a clear function, whether that be ownership, coordination, or leadership.

Financial flows, intra-group relationships, and strategic decisions must reflect tangible economic reality.

The third pillar concerns international compliance.

The structure must comply with applicable anti-abuse rules, as well as the principles of transparency and tax cooperation that now apply to all jurisdictions.

This compliance is not limited to Andorran law, but is also assessed in relation to the relevant foreign legislation.

In the absence of these elements, the theoretical tax benefits may be called into question.

This challenge may be brought by both the Andorran authorities and the tax authorities of the countries where the income is generated or where the shareholders are resident.

The taxation of Andorran holding companies therefore requires a rigorous approach, based on anticipating risks and building a structure that is economically and legally defensible.

III.3. Limitations and points to watch out for

It is important to emphasize one absolutely essential point in any consideration of an Andorran holding company.

Foreign tax authorities never analyze a structure in isolation, nor solely through the lens of the local law under which it is incorporated.

Instead, they examine the Andorran holding company in light of the entire applicable international framework, taking into account tax treaties, OECD principles, and cross-cutting anti-abuse rules.

This comprehensive approach leads to an in-depth analysis of the economic reality, the actual functioning, and the real role of the holding company within the group.

The risks identified in this context are numerous and must be rigorously anticipated.

They primarily concern the questioning of the holding company's effective tax residence.

When the actual place of management or decision-making does not correspond to the state of incorporation, the tax base may be challenged.

Foreign administrations are also focusing on the reclassification of financial flows.

Dividends, interest, royalties, or cash flows may be analyzed from a different perspective than that adopted by the group, with sometimes significant tax consequences.

Furthermore, the application of specific anti-abuse rules or exit tax mechanisms constitutes a significant risk.

These mechanisms are specifically designed to neutralize structures that are perceived as artificial or insufficiently justified economically.

In this context, the analysis of potential tax benefits can never be conducted in isolation.

It must be part of a broader reflection, incorporating the international structure of the group as a whole.

It is equally important to take into account the personal circumstances of executives and shareholders.

Their tax residence, effective decision-making role, and economic interests are key factors in the overall assessment of the arrangement.

It is this cross-disciplinary approach, covering legal, tax, and wealth management aspects, that enables an accurate assessment of the solidity and sustainability of an Andorran holding company in a demanding international environment.

IV. International structuring: cash flows, double taxation, and exit tax

The creation of a holding company in Andorra cannot be analyzed in isolation.

It is necessarily part of an international environment, where financial flows are subject to heterogeneous tax rules.

The challenge is not only tooptimizing, but above all to secure.

IV.1. The nature of cash flows within a holding company structure

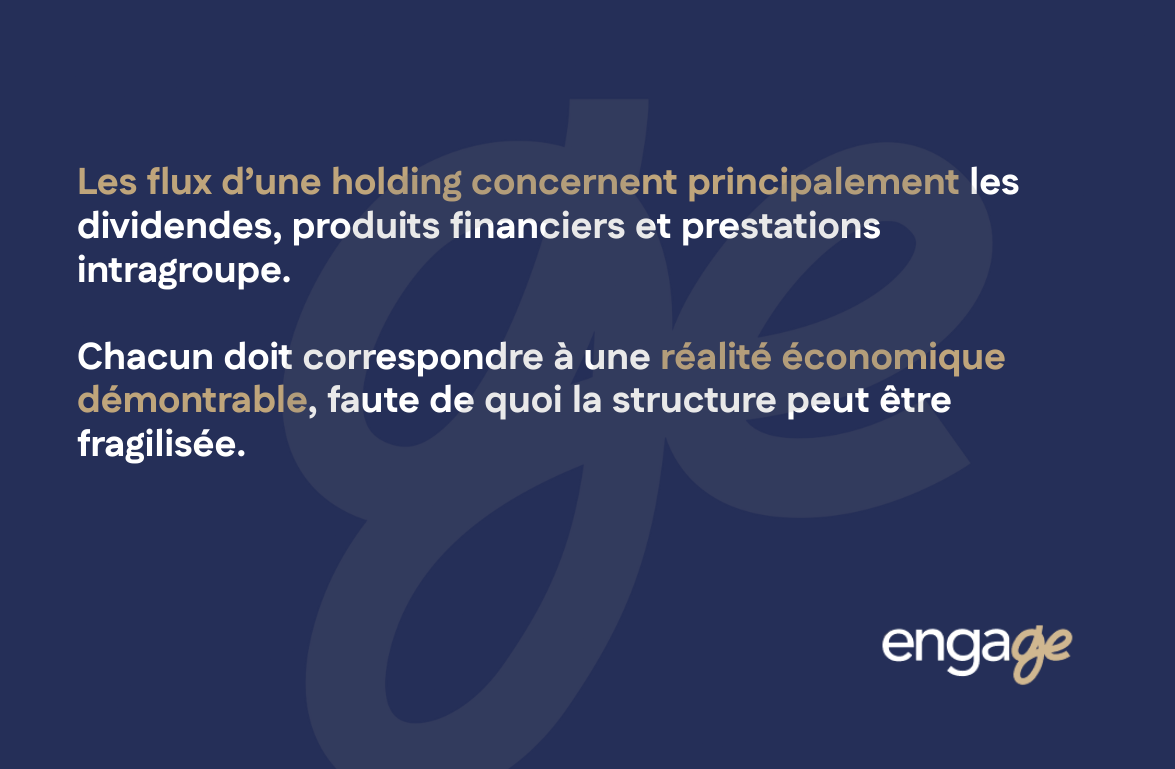

The most frequent flows passing through a holding company fall into clearly identified categories, each of which is subject to particular scrutiny by the tax authorities.

They primarily concern dividends paid by subsidiaries to the holding company.

These flows often form the core of the holding rationale and reflect the upward trend in results generated by operating entities.

They also include financial income from investments made by the holding company.

This may include investment income, financial investments, or cash allocation transactions within the group.

Finally, intra-group flows related to services are playing an increasingly important role in contemporary structures.

They cover management, coordination, administrative or financial assistance services, as well as intragroup financing mechanisms.

Each of these flows is rigorously analyzed by the tax authorities.

The review covers both the economic reality of the transaction, its legal justification, and its consistency with the overall organization of the group.

The amounts invoiced, the calculation methods, and the actual services rendered are decisive factors.

Particular vigilance is required when the holding company merely collects dividends without demonstrating any identifiable structural role.

In such a configuration, the absence of real functions, effective decisions, or added value can weaken the structure.

This risk is heightened when the flows originate from jurisdictions with higher tax rates.

Foreign administrations may then be tempted to question the relevance of the chosen scheme and reclassify its tax effects.

Cash flow management within a holding company cannot therefore be approached passively.

It requires a coherent structure that is well documented and aligned with the group's economic reality, which is essential to the security of the entire system.

IV.2. Withholding taxes and risks of double taxation

The taxation applicable to cross-border flows depends, to a large extent, on the country in which the income is sourced.

Each jurisdiction applies its own rules, which are often complex, regarding the taxation of outbound flows.

In this context, withholding taxes on dividends or interest are one of the main points of friction encountered in international structuring.

They can significantly affect cash flow profitability and undermine the economic balance of a plan that appears coherent on the surface.

The presence of a holding company never automatically neutralizes these withholding taxes.

It does not, in itself, constitute a tax neutralization mechanism that can be enforced against the source countries of the income.

The reduction or elimination of these withholdings depends primarily on the existence of an applicable tax treaty between the source country and the holding company's country of residence.

However, the interpretation and application of these conventions vary significantly depending on the jurisdictions concerned.

A second determining factor is the classification of the company receiving the income.

Tax authorities carefully examine whether the holding company can be regarded as the beneficial owner of the cash flows or whether it acts as a mere conduit entity.

Finally, the absence of artificial or abusive editing is an essential condition.

Any structure perceived as lacking substance or economic justification is likely to be disregarded, regardless of the contractual provisions invoked.

In practice, the analysis of taxation of cross-border flows can never be conducted in an abstract manner.

It must be conducted on a country-by-country basis, taking into account internal rules, applicable conventions, and their practical interpretation.

It is equally essential to take local administrative practice into consideration.

The positions taken by administrations, their degree of vigilance, and their approach to the concepts of substance and beneficial ownership play a decisive role in securing flows.

It is this detailed analysis, covering legal, tax, and pragmatic aspects, that allows for a true assessment of the effectiveness and sustainability of a holding company in a cross-border context.

IV.3. Exit tax and anticipation of future restructuring

The issue of exit tax is often underestimated when setting up a holding company.

Nevertheless, it remains a key issue when the structure is part of an evolutionary trajectory.

This issue becomes particularly sensitive in the event of a change in the tax residence of the director or shareholder.

Moving residence may trigger latent capital gains tax mechanisms, regardless of whether any actual sale takes place.

It also arises during the transfer of securities or assets, whether these are internal transactions within the group or broader restructuring operations.

These asset transfers can trigger complex tax arrangements, which are often insufficiently anticipated.

The issue of exit tax finally comes to a head at the time of a future sale of shares.

The choices made upstream in terms of structuring can then have a decisive impact, either positive or negative, on the taxation applicable at the time of exit.

In this context, a holding company can be a useful tool for anticipating and managing such situations.

When designed from the outset with a long-term perspective, it allows for the organization of asset holdings and preparation for future developments within a controlled framework.

However, this efficiency assumes that the structure has been designed in advance, incorporating assumptions about mobility, transfer, or disposal.

A reactive or delayed approach significantly limits the room for maneuver.

Otherwise, the holding company may, on the contrary, crystallize significant tax risks at the time of exit.

Once triggered, exit tax mechanisms leave little room for adjustment and can generate significant costs.

Anticipation thus appears to be a key factor in the use of a holding company, ensuring that it remains a tool for security rather than a source of rigidity or risk.

V. Tax residence of executives and shareholders: risk areas

The taxation of a holding company in Andorra cannot be separated from the personal situation of those who control it.

The tax residence of executives and shareholders is a determining factor in the overall assessment of the structure.

V.1. The concept of effective management

A company's tax residence is largely based on the location where strategic decisions are actually made.

It cannot be deduced from a registered address or the simple location of a formal head office.

The concept of effective management is a key criterion in this regard, assessed in concrete terms by the tax authorities.

The authorities do not limit themselves to examining the articles of association or incorporation documents, but focus on the actual functioning of the company.

In this analysis, several factual elements are taken into consideration.

The composition of decision-making bodies is subject to careful scrutiny, particularly in order to identify those individuals who wield real power.

The frequency and location of meetings of governing bodies are also key indicators.

Administrations seek to determine where structural decisions are prepared, debated, and finalized.

Finally, the identity of the persons who actually exercise management authority is of particular importance.

It is a matter of identifying who drives the strategy, who makes the key decisions, and who takes responsibility for the choices made.

Increased vigilance is required when the same individuals hold both the decision-making power of the holding company and their tax residence in another jurisdiction.

The confusion between the personal residence of executives or shareholders and the tax residence of the holding company is one of the main factors calling this into question.

In such situations, the authorities may consider that effective management is exercised outside Andorra, with potentially serious tax consequences.

The structure of governance therefore appears to be a determining factor in securing the tax residence of a holding company.

V.2. Personal residence and holding company: a sensitive issue

When directors or shareholders reside in another state, the tax authorities of that state may be tempted to consider that the holding company is, in fact, managed from their own territory.

This analysis is based on a factual approach, focused on the actual exercise of decision-making power.

The risk is particularly high when all strategic decisions are concentrated in the hands of a single person.

Such a configuration weakens the argument that the holding company has a separate and independently located effective management.

It is also reinforced when the holding company does not have its own clearly identified and functional governance structure.

The absence of active decision-making bodies, internal rules, or formalized processes fuels the idea of a purely formal structure.

Finally, the lack of real substance is a major aggravating factor.

Without human resources, operational organization, or demonstrable decision-making activity, the holding company struggles to justify its tax base.

Under these circumstances, foreign tax authorities may be led to reclassify the place of effective management.

Such a reclassification has significant tax consequences for both the company and its shareholders.

The holding company must therefore never appear to be a simple extension of the assets of the individual who owns or controls it.

On the contrary, it must embody a distinct entity, with autonomous governance and a coherent economic reality.

It is this clear separation between the individual and the company that makes it possible to secure the holding company's tax residence on a long-term basis.

V.3. Practical security measures for tax residence

Securing a holding company relies on a combination of complementary factors, which must be considered in a consistent and sustainable manner.

First and foremost, it requires a clear organization of powers within the structure.

Roles and responsibilities must be clearly defined in order to unambiguously identify the bodies and individuals vested with decision-making authority.

Effective governance is the second pillar of this security.

It implies the existence of real decision-making mechanisms that are regularly implemented and duly documented.

Meetings, decisions, and strategic directions must be traceable and justified in a consistent manner.

Overall consistency between discourse, behavior, and operational reality ultimately appears to be a determining factor.

Formal statements must correspond to actual practices, both in the conduct of business and in the day-to-day organization of the holding company.

It is not a question of multiplying artifices or creating an appearance of substance disconnected from reality.

Purely formal arrangements are particularly vulnerable to challenge today.

The objective is, on the contrary, to build a credible structure that is clear and consistent with its actual function.

It is this authenticity, based on the alignment of the legal form with the economic reality, that provides lasting security for the holding company and its tax environment.

VI. Tax treaties and international structuring: what you really need to check

Tax treaties are often presented as a key factor in the attractiveness of a jurisdiction.

However, their role must be analyzed with caution.

VI.1. The actual scope of tax treaties

The main purpose of a tax treaty is to avoid double taxation and to allocate the right to tax between the states concerned.

It is a tool for coordination between national tax systems, designed to prevent conflicts of jurisdiction and double taxation.

However, it does not, on its own, create a right totax optimization.

Its existence does not guarantee either an automatic advantage or systematic neutralization of taxation in either State.

The application of an agreement depends primarily on the classification of the income concerned.

The legal and economic nature of the flows determines the applicable treaty provisions and the terms and conditions for allocating the right to tax.

A second essential criterion is the effective residency status of the company or person invoking the agreement.

Tax authorities carefully examine the reality of the claimed residence and the place of effective management.

Compliance with conventional anti-abuse clauses is ultimately a decisive factor.

These clauses are specifically designed to rule out artificial or insubstantial arrangements, even when the formal conditions appear to be met.

Thus, a tax treaty cannot be considered in isolation.

Its benefit requires a rigorous analysis of cash flows, the structure that receives them, and the overall consistency of the arrangement.

It is on this condition that conventional application can be part of a secure and legally defensible approach.

VI.2. Practical limitations in a holding company context

In a holding company context, foreign tax authorities conduct a particularly careful analysis of the structure that claims treaty treatment.

They do not simply verify the formal existence of a company or the apparent compliance of documents.

They first examine the substance of the company receiving the income.

The question is not only where the holding company is registered, but whether it has an economic reality, organization, and governance consistent with its function.

Human resources, decision-making capacity, and the traceability of strategic choices are key indicators in this regard.

They then focus on the absence of artificial intermediation.

When a holding company appears to be merely a conduit for capturing cash flows without performing any real function, the conventional benefit may be challenged.

This assessment is based on the functions performed, the risks assumed, and the demonstrable economic utility of the company in the detention chain.

Finally, they analyze the consistency of the detention chain as a whole.

The structuring logic must be clear, stable, and justifiable in light of the objectives pursued.

Breaks in consistency, unnecessary steps, or structures with no identifiable function weaken the entire structure.

A purely theoretical reading of tax treaties is therefore insufficient.

Texts must be interpreted in light of administrative practice and relevant case law decisions.

These concrete elements guide the way in which administrations apply the concepts of effective residence, beneficial owner, and anti-abuse clauses.

This is why conventional analysis must be conducted methodically, taking into account all the factual context and the applicable legal environment.

VI.3. The importance of cross-border coordination

The structuring of a holding company very often involves the intervention of several jurisdictions, each applying its own rules and developing its own interpretations.

In such a context, a compartmentalized approach, limited to the analysis of a single country, constitutes a major source of risk.

The lack of coordination between different national interpretations can lead to legal or tax inconsistencies, which can sometimes be difficult to correct retrospectively.

Coordination between the councils involved in each country therefore appears to be a key factor in ensuring security.

First and foremost, it allows for the anticipation of differences in interpretation that may arise between tax authorities.

The concepts of residence, substance, or beneficial owner may be understood differently depending on the jurisdiction.

This coordination also facilitates the alignment of legal and tax structures at the international level.

The choices made in one country must be compatible with the requirements and practices of the other States concerned.

Finally, it helps to reduce areas of uncertainty.

By cross-referencing analyses and comparing points of vigilance, it becomes possible to build a more robust and readable structure.

International consistency is therefore not the result of a juxtaposition of local solutions.

It requires a comprehensive vision, supported by constant dialogue between the various councils involved in the project.

VII. Shareholder agreements and governance: securing control and strategy

The contractual aspect is often overlooked when setting up a holding company.

However, shareholder agreements play a decisive role in the stability and sustainability of the structure.

VII.1. The strategic role of agreements in a holding company

A shareholder agreement allows the relationships between partners to be organized precisely and in advance.

It supplements the articles of association to regulate essential aspects of the company's life.

First and foremost, it allows for the structuring of capital control.

The terms of ownership, the balance between partners, and the mechanisms for protecting minority interests can be defined with precision.

The pact also sets out the rules of governance.

It specifies the distribution of powers, the conditions for decision-making, and the balance between the various bodies.

This clarification contributes to the stability of the holding company's operations and helps prevent deadlock situations.

Finally, it sets out the terms and conditions for the entry and exit of partners.

The terms of sale, preemptive rights, and joint or forced exit clauses make it possible to anticipate changes in capital.

In the context of a holding company, the shareholder agreement is therefore an essential tool for predictability.

It offers greater visibility on the future evolution of the structure, both for entrepreneurs and for wealth-holding families.

This predictability promotes project continuity, secures transfers, and strengthens long-term governance consistency.

VII.2. Structural clauses

Among the most common clauses found in a shareholders' agreement, some play a central role in the organization of a holding company.

They enable sensitive situations to be anticipated and ensure harmony between partners.

Preemption clauses are intended to regulate the transfer of securities.

They offer existing partners priority in acquiring the shares or units offered for sale, thereby contributing to shareholder stability.

The purpose of inalienability clauses is to limit, for a specified period, the possibility of transferring securities.

They are frequently used to ensure project consistency or maintain control over capital in the early stages of structuring.

Liquidity mechanisms also play an important role.

They make it possible to organize the conditions under which a partner can leave the holding company or, conversely, be forced to sell their shares.

These mechanisms help prevent deadlock situations and provide clear prospects in the event of changes in capital.

Finally, the rules for strategic decision-making are a key element of the pact.

They determine the decisions requiring enhanced agreement and define the balance of power within the holding company.

All of these clauses must be adapted to the actual function of the holding company.

A family or management holding company does not require the same mechanisms or the same degree of flexibility.

The envisaged holding period is also a decisive factor.

The clauses must be designed in line with long-term objectives in order to ensure the clarity and sustainability of the structure.

VII.3. Family agreements and investor agreements

The objectives pursued vary significantly depending on whether the holding company is family-owned or open to external investors.

This distinction directly influences the philosophy of the shareholders' agreement and the mechanisms it contains.

The family pact is primarily geared toward capital stability.

It aims to organize long-term care, facilitate the transition, and preserve the balance between family members.

Conflict prevention is a key issue, particularly through the clarification of governance rules and decision-making procedures.

The investor pact follows a different logic.

It prioritizes the liquidity of holdings and the precise definition of investors' rights and obligations.

Governance is often structured in a more formalized manner in order to secure strategic decisions and control mechanisms.

Exit scenarios play a key role in this context.

The terms of transfer, joint or forced exit rights, and liquidity horizons are defined from the outset.

In all cases, the relationship between the agreement and the holding company's articles of association must be carefully considered.

The two instruments must be consistent, complementary, and legally secure.

Any contradiction or inaccuracy can weaken the entire structure and cause difficulties during implementation.

VIII. Real estate and holding companies in Andorra: opportunity or false good idea?

Real estate often plays a central role in private wealth.

It is therefore natural that the question of its ownership via an Andorran holding company should arise.

However, this structure warrants a particularly nuanced analysis.

VIII.1. Real estate ownership via a holding company: apparent logic

Holding real estate through a holding company can serve several structural purposes, both in terms of assets and organization.

First and foremost, it allows for the centralization of asset ownership within a single entity.

This centralization makes it easier to understand the assets and provides a consolidated view of the property owned.

It can also facilitate the transfer by organizing the transfer of the holding company's securities rather than the real estate itself.

This approach often offers greater flexibility, both legally and operationally.

The holding company is also a useful tool for organizing family governance around real estate assets.

It allows decision-making rules to be defined, powers to be distributed, and generational changes to be anticipated within a structured framework.

Another common objective is to separate financial risks.

By isolating real estate within a holding company, it becomes possible to limit the direct exposure of individuals and better control legal and financial risks.

Conceptually, the holding company thus appears to be a tool for streamlining real estate ownership.

It offers a clear architecture that can address issues related to the management, transmission, and protection of heritage.

In practice, however, the relevance of this model depends heavily on several parameters.

The type of real estate asset concerned, its geographical location, and the applicable legal and tax regime are determining factors.

The envisaged heritage horizon also plays a central role.

A long-term holding does not call for the same choices as a project involving a medium-term sale or restructuring.

Real estate ownership via a holding company cannot therefore be approached in a standardized manner.

It requires a detailed analysis tailored to the characteristics of the asset and the wealth management objectives pursued.

VIII.2. Analysis by asset objective

Long-term returns and holding

When the primary objective is to generate rental income, owning real estate through a holding company should be considered with caution.

This structure may introduce an additional layer of taxation, as well as increased legal, accounting, and administrative obligations.

In many cases, these constraints do not come with any obvious economic advantage, particularly when the wealth management strategy is based on long-term asset preservation.

The holding company can then complicate ownership without significantly improving the net return received by the partners.

Transmission

The transfer of shares in a company that owns real estate may, from a legal standpoint, appear to be more flexible than the direct transfer of the property itself.

This flexibility is often sought after in a family context, particularly for organizing a gradual transfer or distributing rights among several beneficiaries.

However, this theoretical advantage must be weighed against the rules applicable in the country where the property is located.

Transfer taxes, civil law rules, and local tax provisions may significantly limit the effectiveness of the proposed scheme.

Resale and liquidity

The issue of liquidity is another major point of concern.

The sale of shares in a company whose main activity is real estate is not automatically treated, for tax purposes, as the sale of the underlying real estate.

This distinction is particularly significant in light of anti-abuse rules and applicable local tax laws.

Some jurisdictions treat the transfer of securities as an indirect real estate transfer, with equivalent or even greater tax consequences.

Resale via a holding company therefore guarantees neither tax neutrality nor increased liquidity.

It must be assessed in light of local rules, administrative practice, and overall asset strategy, in order to avoid any illusion of simplification or automatic optimization.

VIII.3. A structure to be handled with care

In many cases, holding real estate through an Andorran holding company is neither the simplest nor the most efficient solution.

The apparent elegance of the scheme should not obscure the legal, tax, and operational constraints it may entail.

The superimposition of levels of detention can unnecessarily complicate the structure without providing a proportionate benefit in relation to the objectives pursued.

This increased complexity can result in less clarity in the arrangement, both for the partners and for the tax authorities concerned.

In certain configurations, separate structures may offer a better match between the real estate asset and its legal ownership.

They sometimes enable a more direct response to issues relating to heritage management, transmission, or protection, while limiting areas of uncertainty.

Hybrid schemes may also be considered.

They involve combining several legal tools, taking into account the nature of the assets, their location, and the chosen asset horizon.

These alternative approaches often offer greater legal certainty and better economic consistency.

They make it possible to avoid standardized setups and adapt the structure to the specific realities of the heritage project.

Real estate ownership must therefore be approached pragmatically.

The objective is not to use a holding company as a matter of principle, but to choose the structure that is the most transparent, the most defensible, and the most appropriate for the situation in question.

IX. Andorran holding companies and international financial investments

Beyond real estate, the holding company can play a structuring role in the organization of diversified financial investments.

IX.1. Centralization and management of investments

A holding company allows a wide variety of financial assets to be centralized within a single structure.

It may include investments in equities, whether in listed or unlisted companies.

This centralization facilitates performance monitoring and the allocation of investments within a portfolio approach.

It may also hold interests in investment funds.

Whether specialized funds, private equity vehicles, or more diversified structures, the holding company provides a unified framework for their ownership.

The holding company can finally accommodate diversified financial products.

Financial investments, cash instruments, or more sophisticated investments can be organized within a single structure.

This centralization offers a major advantage in terms of management.

It provides a comprehensive overview of financial assets, without dispersion between different entities or direct holdings.

The consolidated view provided by the holding company facilitates strategic decision-making.

Investment, divestment, or asset reallocation decisions can be made in a more consistent and transparent manner.

The financial holding company is therefore an organizational and management tool, provided that its establishment is based on a clearly defined asset management strategy.

IX.2. Investment discipline and economic justification

The use of a holding company as an investment vehicle requires real and constant discipline in its operation.

It cannot be limited to a simple tool for passive detention without a framework or method.

A defined investment policy is the first key element.

The general guidelines, preferred asset classes, and objectives must be clearly identified and formalized.

This preliminary definition allows decisions to be made in a consistent and sustainable manner.

The traceability of decisions is a second imperative.

Every decision, every investment, and every divestment must be traceable and justifiable.

Decisions made must be documented, both to ensure good internal governance and to meet the requirements of tax authorities.

Finally, consistency between strategy and financial flows is a decisive factor.

Cash flows must reflect the announced strategy and correspond to actual, economically justified transactions.

Without this rigor, the holding company risks appearing to be nothing more than an intermediary investment account.

Such a perception weakens its economic justification and exposes the structure to questioning.

The investment holding company must therefore be designed and managed as a separate entity, with its own logic and effective governance, in order to preserve its credibility and legal certainty.

IX.3. Compliance and banking relationships

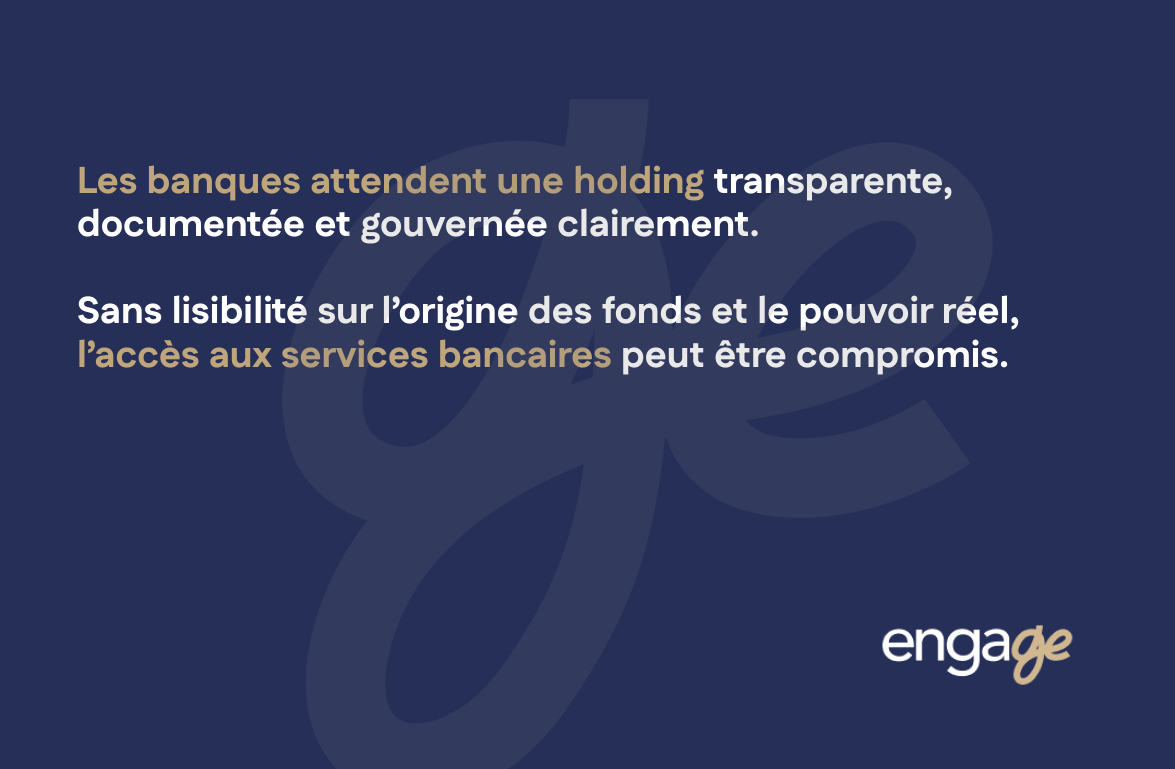

Financial institutions pay particular attention to the transparency of holding company structures.

In an environment marked by increased compliance requirements, banks conduct in-depth analyses of the legal and asset structures presented to them.

Clear documentation is an essential prerequisite.

The articles of association, any agreements, ownership charts, and governance documents must provide an immediate understanding of the structure and how it operates.

Any gray areas or inconsistencies in documentation can weaken the banking relationship.

Transparent governance is another key factor.

Financial institutions seek to accurately identify decision-making bodies, individuals exercising real power, and internal control procedures.

Structured and consistent governance enhances the credibility of the holding company.

Finally, the origin of the funds must be fully justified.

The traceability of contributions, financial flows, and investments is a major point of vigilance in the context of anti-money laundering and counter-terrorist financing obligations.

Without this transparency, access to banking services can become complex or even be called into question.

The holding company may then find itself facing operational restrictions that are incompatible with its objectives.

The quality of the banking relationship is therefore based on a rigorous structure that is understandable and complies with current compliance standards.

This is the price that must be paid to establish and maintain lasting and secure banking relationships.

X. Family asset organization: governance and control

The holding company comes into its own when it is part of a long-term family strategy.

X.1. Structuring power and decision-making

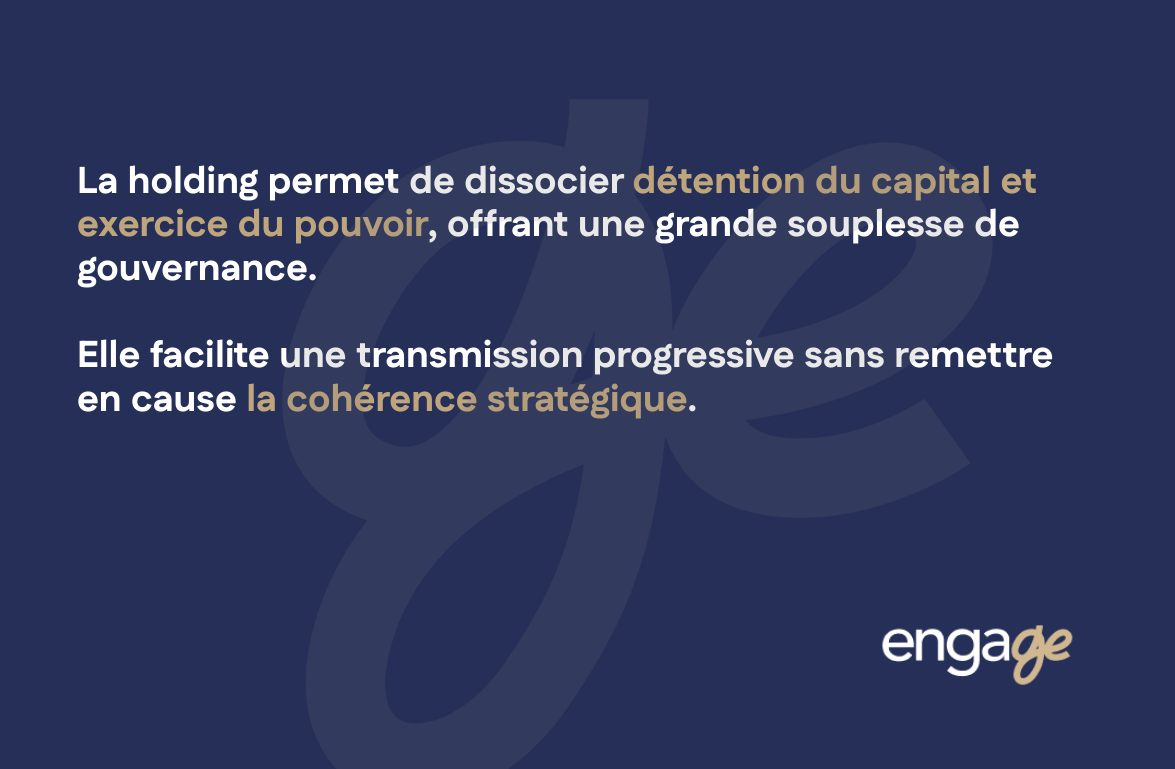

The holding company makes it possible to separate several key aspects of wealth and business organization.

First, it distinguishes between economic ownership of assets and the exercise of decision-making power.

This separation offers great flexibility in the allocation of rights and responsibilities.

It also makes it possible to differentiate between the exercise of power and operational management.

Strategic management functions can be concentrated at one level, while day-to-day operations are entrusted to other actors.

This structured separation is a particularly effective lever for supporting a group's development over time.

It facilitates the gradual integration of subsequent generations without compromising the overall balance of the structure.

New entrants may be involved in capital or governance on a gradual and controlled basis.

At the same time, the overall strategic consistency is maintained.

The fundamental guidelines remain clear, the decision-making centers have been identified, and continuity of choices is assured.

The holding company thus establishes itself as a tool for transfer and evolving governance, enabling generational renewal and strategic stability to be combined.

X.2. Preventing family conflicts

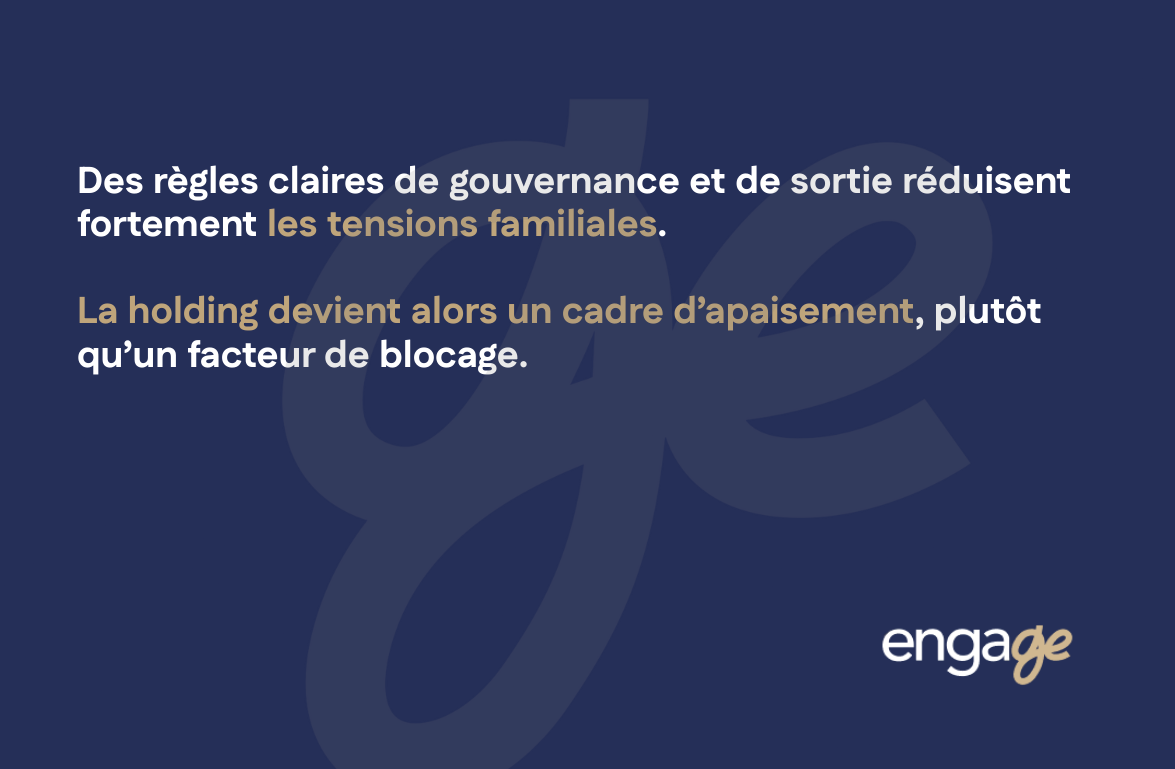

The lack of clear rules is one of the main sources of tension in family and patrimonial organizations.

When roles, powers, and expectations are not formalized, differences in interests or perceptions can quickly turn into long-lasting conflicts.

In this regard, the holding company provides a structured framework for formalizing the rights and obligations of each party.

It allows for the precise definition of the prerogatives attached to the ownership of capital, as well as the corresponding commitments of the partners.

It also provides an effective tool for organizing decision-making processes.

Governance rules, majority thresholds, and strategic decisions requiring enhanced consensus can be clearly identified.

This formalization contributes to smooth operations and prevents bottlenecks.

Finally, the holding company makes it possible to anticipate and manage exit mechanisms.

The conditions under which a partner may withdraw, transfer their shares, or be bought out are defined in advance.

This foresight limits crisis situations and provides valuable insight into the future development of the structure.

By providing a clear and shared framework, the holding company helps to smooth out inheritance issues and ensure the long-term viability of the collective project.

X.3. Continuity and asset stability

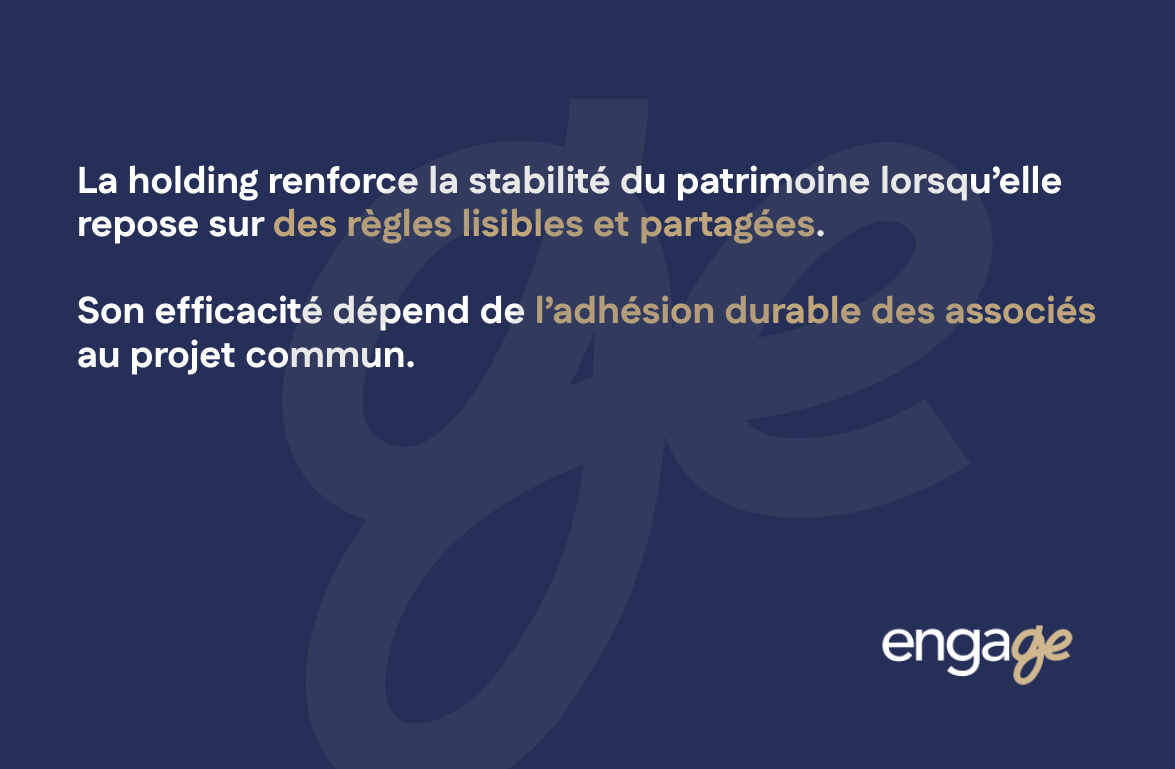

Designed as a genuine governance tool, the holding company can play a decisive role in the stability of family assets.

It provides a structured framework for organizing powers, anticipating changes, and preventing imbalances that may arise over time.

However, this contribution to stability is only effective if the rules have been clearly defined in advance.

Governance principles, decision-making mechanisms, and the balance between the parties must be formalized in a clear and consistent manner.

It is equally essential that these rules are understood and accepted by all those concerned.

The support of partners, and in particular family members, determines the legitimacy and effectiveness of the system.

Under this condition, the holding company becomes an instrument of continuity and appeasement, serving a shared and sustainable heritage project.

XI. Transmission, protection, and liquidity

The issue of inheritance is inseparable from any estate planning.

XI.1. Anticipating transmission

Holding securities in a holding company can be a particularly effective way of organizing the transfer of assets over time.

It allows for gradual transfers, adapted to the family's pace and changing personal circumstances.

This gradual approach promotes the controlled integration of beneficiaries, without any sudden disruption to the balance of assets.

The holding company also facilitates the implementation of organized donations.

The transfer of securities, rather than underlying assets, often offers greater legal flexibility and greater transparency of transactions.

It allows for the separation of economic transmission from the exercise of power, according to precisely defined terms.

The distribution of assets can thus be planned in a detailed and controlled manner.

Financial rights, voting rights, and control mechanisms can be arranged to meet family and estate planning objectives.

Anticipation plays a decisive role here.

It is essential for securing tax matters, taking into account the rules applicable at the time of transfer.

It is equally important on a family level, helping to prepare beneficiaries, clarify intentions, and limit potential sources of tension.

When planned and structured in advance, holding securities becomes a flexible, transparent, and sustainable tool for transferring assets as part of a well-thought-out wealth management strategy.

XI.2. Protection of spouse and heirs

The holding company can be integrated into an overall asset protection strategy, provided that it is viewed as one tool among many and not as a stand-alone solution.

Its effectiveness depends on its ability to work harmoniously with the applicable inheritance rules.

The detention arrangements put in place at the holding company level must be compatible with the relevant inheritance law, whether national or international.

Otherwise, the structure may encounter legal constraints that could limit its scope or undermine its stability.

It is equally essential that the holding company reflects the family's actual objectives.

The protection sought may be aimed at preserving assets, ensuring continuity of governance, or maintaining balance among heirs.

These objectives must be clearly identified and reflected in the chosen structure.

The holding company does not constitute protection in itself.

It only becomes protective when it is integrated into a comprehensive, coherent, and forward-looking approach.

It is through this combination of legal tools, inheritance rules, and family plans that the holding company can fully play its role in ensuring the stability and longevity of the family's assets.

XI.3. Liquidity and exit scenarios

A relevant structure must always incorporate realistic and accepted liquidity assumptions from the outset.

Heritage is never completely static, and any sustainable organization must plan for scenarios of change.

Partial disposal is one such scenario.

It can meet a need for asset reallocation, financing, or adaptation of the wealth management strategy.

The structure must allow for this flexibility without throwing the whole thing off balance.

The departure of a partner is another common situation.

Whether chosen or forced, it must be able to operate according to pre-established rules, avoiding tensions and blockages.

Anticipating exit arrangements contributes directly to the stability of the group.

Gradual divestment should also be considered.

It allows for a gradual reduction in equity exposure, particularly when a transfer or change in life cycle is approaching.

The holding company must not therefore have the effect of freezing assets.

On the contrary, it must offer options, flexibility, and room for maneuver.

It is this ability to adapt, built into the structure from the outset, that guarantees the holding company's relevance and longevity over time.

XII. Decision-making methodology: when to set up (or not set up) a holding company in Andorra

The key question is not whether a holding company in Andorra is attractive, but rather whether it is appropriate in the circumstances.

Perceived attractiveness is never a sufficient criterion.

Only when the legal tool is appropriate for the objectives pursued can the soundness of a structure be assessed.

XII.1. Cases in which the holding company may be appropriate

A holding company can be useful in the context of international business activities.

The presence of subsidiaries or investments in multiple jurisdictions often justifies a centralized structure and governance.

It also has its place when the estate is diversified and already structured.

The holding company then makes it possible to organize, manage, and arbitrate different types of assets in a consistent manner.

A long-term horizon is another key criterion.

A holding company is a tool for building sustainable wealth, which is not really compatible with opportunistic or short-term thinking.

Finally, a clear commitment to organized governance reinforces the relevance of using a holding company.

When partners wish to formalize rules for decision-making, control, and transfer, a holding company offers a suitable structural framework.

XII.2. Risky or inappropriate situations

However, certain configurations make the use of a holding company particularly fragile.

The absence of possible substance is a primary factor in maladjustment.

Without real resources, effective governance, or an identifiable role, the holding company becomes difficult to defend.

An exclusively tax-related objective also exposes the structure to high risks.

Arrangements that lack economic justification are now systematically challenged.

An overly simple structure may also not justify setting up a holding company.

When asset holdings are limited and do not change much, the resulting complexity may outweigh the expected benefits.

Finally, uncontrolled international constraints are a major vulnerability factor.

The lack of a cross-functional vision exposes the organization to inconsistencies and multiple challenges.

XII.3. Preliminary strategic checklist

Before making any decision, a thorough analysis is required.

The actual objectives pursued must be clearly identified.

This clarification determines all structural choices.

The personal circumstances of managers must be carefully examined.

Tax residence, decision-making role, and economic interests directly influence the robustness of the scheme.

The location of assets is another key parameter.

Each jurisdiction imposes its own legal and tax constraints.

The heritage horizon must be clearly defined.

Transmission, preservation, or transfer do not require the same choices.

Finally, the ability to maintain credible governance over time must be assessed without complacency.

It is only after this comprehensive analysis that the relevance of a holding company in Andorra can be assessed with clarity and rigor.

XIII. Operational implementation: steps, costs, and discipline

The creation of a holding company is never an end in itself.

On the contrary, it marks the starting point of a structuring process that is set to continue over the long term.

The relevance of the holding company is not judged solely at the time of its formation, but also in terms of its ability to function, evolve, and remain consistent over time.

XIII.1. Creation and initial structuring

The implementation phase is of crucial importance.

It begins with the choice of legal form, which must be suited to the nature of the project, the type of partners, and the objectives pursued.

This choice determines the legal framework, governance, and future flexibility of the structure.

Defining the corporate purpose is an equally essential step.

An overly narrow scope limits the holding company's development, while an excessively broad scope can undermine its clarity and economic justification.

Balance must be sought from the outset.

The governance structure must then be carefully thought out.

The distribution of powers, decision-making procedures, and control mechanisms must reflect the reality of the intended operation.

This initial governance lays the foundations for the holding company's future credibility.

The opening of banking relationships is finally a major operational milestone.

It requires clear documentation, a transparent structure, and complete transparency regarding the origin of funds and the organization of the group.

XIII.2. Recurring costs and obligations

By its very nature, a holding company generates recurring costs that must be anticipated.

The accounting costs associated with maintaining accounts, preparing financial statements, and fulfilling reporting obligations are incompressible.

Legal costs must also be taken into account.

They concern both the day-to-day management of the company and the adaptation of articles of association, agreements, or intra-group agreements.

Administrative obligations add to these burdens.

They require rigorous organization and constant attention to deadlines and formalities.

Finally, compliance requirements are becoming an increasingly important area of focus.

Transparency, documentation, due diligence obligations, and information sharing are now an integral part of the life of a holding company.

All of these elements must be included in the overall profitability analysis from the outset.

A holding company is only relevant if its costs and constraints are proportionate to the expected benefits.

XIII.3. Long-term governance

The value of a holding company is measured above all over time.

It relies on continuous discipline and the ability to maintain consistency between the legal structure and economic reality.

This sustainable governance requires regular adaptation to regulatory and tax changes.

The applicable rules are changing, sometimes rapidly, and require constant adjustments.

It also requires constant vigilance with regard to the actual functions performed by the holding company.

The structure must remain faithful to its role, without drifting or gradually disconnecting from its original purpose.

It is through this continuity, characterized by rigor, adaptability, and consistency, that the holding company maintains its legitimacy and value as a tool for wealth and business organization.

Conclusion

A holding company in Andorra is neither a standardized arrangement nor a universal solution that can be applied indiscriminately to all situations.

It is a demanding structuring tool, whose relevance depends exclusively on the quality of the upstream thinking and the consistency of its practical implementation.

It only makes sense when it is part of an overall vision that incorporates the legal, tax, asset, and human aspects of the proposed project.

The formal existence of a holding company cannot, on its own, produce beneficial effects.

When used rigorously, methodically, and judiciously, a holding company can become a powerful tool for wealth management.

It helps to structure entrepreneurial activity, clarify roles within a group, and prepare for the future with a view to continuity and stability.

It can also provide a relevant framework for anticipating transfers, organizing governance, and supporting generational changes without disruption.

Conversely, if poorly designed or insufficiently thought out, the holding company quickly becomes a source of unnecessary complexity.

This exposes its beneficiaries to legal, tax, and operational risks that can sometimes be difficult to control after the fact.

Artificial structures, lacking substance or economic coherence, are particularly vulnerable today.

The true value of a holding company therefore does not lie in an isolated analysis of its tax regime.

It is measured by its ability to organize, secure, and pass on a heritage and entrepreneurial project over time.

It is this long-term vision, based on consistency, governance, and economic reality, that gives the holding company its legitimacy and real usefulness.

Are you considering setting up a holding company in Andorra or would like to reevaluate an existing structure in light of your current situation.

Each heritage and entrepreneurial project presents specific challenges that cannot be addressed through standardized approaches.

A personalized analysis makes it possible to identify relevant levers, anticipate risks, and build a coherent, defensible, and sustainable structure.

Our approach is based on a cross-disciplinary analysis, incorporating taxation, corporate law, governance, and international constraints.

It aims to secure your decisions and align the chosen structure with your actual, present, and future objectives.

To take things further, we invite you to contact us so that we can engage in a structured and confidential discussion about your project.

An in-depth discussion is often the first decisive step toward a well-managed estate and business organization.