Setting up a holding company in Andorra: strategic guide to tax optimization and asset structuring

Introduction

Setting up a holding company in Andorra is never a simple technical matter.

It is a structural decision that affects governance, cash flow, legal certainty, and, very often, the ability to organize assets over the long term.

Andorra's appeal is real: a stable institutional framework, modern corporate law, and competitive taxation.

But this attractiveness is too often presented as a ready-made, almost automatic solution.

However, an Andorran holding company is neither universal nor magical.

Its relevance depends on the objectives pursued, the nature of the assets, the profile of the decision-makers, and the international environment in which the structure operates, in a context of increased fiscal transparency.

This article makes a clear promise: to provide you with a strategic, asset-based, and tax-related framework for assessing, with discernment, whether a holding company in Andorra is relevant, sustainable, and defensible in your situation.

As a bonus, you will have access to a comparative tax simulator, designed as an educational and decision-making tool, allowing you to compare the effects of structuring via a holding company in Andorra with other jurisdictions such as France, Spain, the United Kingdom, Germany, and other countries as appropriate.

To get to the point, the full article, which also includes the simulator, is available to help you gain a deeper understanding of the challenges facing a holding company in Andorra.

If you are considering setting up a holding company in Andorra or reevaluating an existing structure, ENGAGE can assist you with a structured and confidential analysis to align your wealth and business organization with your real and long-term goals.

Finally, you can approach the text of this article as a guide à la carte based on the outline provided.

I. What is a holding company (and what it is not)

Understanding a holding company means understanding a management tool, not a recipe.

Its real value lies in the way it structures control, flows, and risks.

Your first decision is therefore not "where to implement it," but "what purpose it serves, specifically, in your wealth management architecture."

The economic function of a holding company is primarily to hold equity interests and centralize decision-making power.

The logic of centralization provides a consolidated view, which is useful for arbitrating, investing, financing, or reallocating capital.

The governance dimension allows for the creation of a strategic level, where rules, mandates, and sometimes the separation of roles are formalized.

The financial function becomes relevant when the holding company organizes dividend payments, intra-group financing, or group cash management.

Heritage protection can also be strengthened, not by magic, but by intelligently separating operational risks and assets.

The fundamental limitation remains that the holding company does not "create" value in itself, and that it must be justified by its usefulness.

The main typologies determine the level of requirement and the economic narrative that you will need to support.

- A pure holding company limits itself to ownership, which may be consistent in terms of assets, but requires increased vigilance with regard to substance and overall logic.

- The holding company actively intervenes, coordinates, provides internal services, and often strengthens economic credibility if the role is real and documented.

- The asset holding company serves to organize long-term ownership, establish family rules, and prepare for transfers.

The right choice depends less on vocabulary than on facts: functions performed, decisions made, resources implemented, and consistency with the objective.

It is important to clearly state what the holding company does not allow, because that is where costly mistakes arise.

- It does not eliminate taxation in countries where income is generated, nor withholding taxes, nor anti-abuse analyses.

- It does not replace the study of the tax residence of executives and shareholders, which remains a key security measure.

- It does not preclude possible reclassifications if the structure appears artificial or disconnected from economic reality.

- It never dispenses with demonstrable governance, consistent flows, and careful documentation.

II. Why Andorra: legal, economic, and tax considerations

Choosing Andorra should not be a tax reflex, but an ecosystem choice.

The real question is whether the Principality fits in with your group's logic, your personal trajectory, and your international constraints.

Andorra's key advantage lies in the combination of institutional stability, modern laws, and structured taxation, in a context that is now highly regulated.

Andorra's position within Europe is unique because it combines sovereignty with gradual integration into international standards.

The regulatory transformation that has been underway for several years has strengthened information sharing, transparency, and compliance.

The change in perception is significant, as Andorra is no longer viewed as a "gray area," but rather as a jurisdiction that expects consistency and substance.

The practical consequence is immediate: an Andorran holding company must be considered a real, governed, and traceable entity.

The historical caricature of easy optimization therefore becomes a risk, because it leads to fragile structures.

Economic logic can be entirely consistent in certain strategies.

Centralizing international holdings can improve transparency, governance, and arbitration capacity at the group level.

Structuring an entrepreneurial group within a stable framework can facilitate internal organization, financing, and growth management.

Organizing family assets can find stability in a holding company, provided that true management discipline is exercised.

Preparing for a sale or transfer may also justify upstream structuring, which is more transparent and proactive.

The decisive factor remains the alignment between advertised functions and operational reality, because that is where defensibility comes into play.

Who Andorra appeals to depends less on desire than on the ability to maintain the structure over time.

International profiles often find this to be a useful tool if multi-jurisdictional ownership requires a clear group leader.

Wealthy families can see this as a framework for governance, continuity, and transfer, provided that the rules are established and accepted.

Structured investorscan centralize assets there, but will have to accept banking and compliance requirements.

Domestic structures without a cross-border dimension often have little to gain and much to complicate.

Short-term or purely tax-related motivations weaken the structure, because they are the first to be targeted by anti-abuse interpretations.

III. The tax advantages of a holding company in Andorra: reality, scope, and conditions

When discussing tax benefits, it is important to distinguish between theory, conditions, and risk.

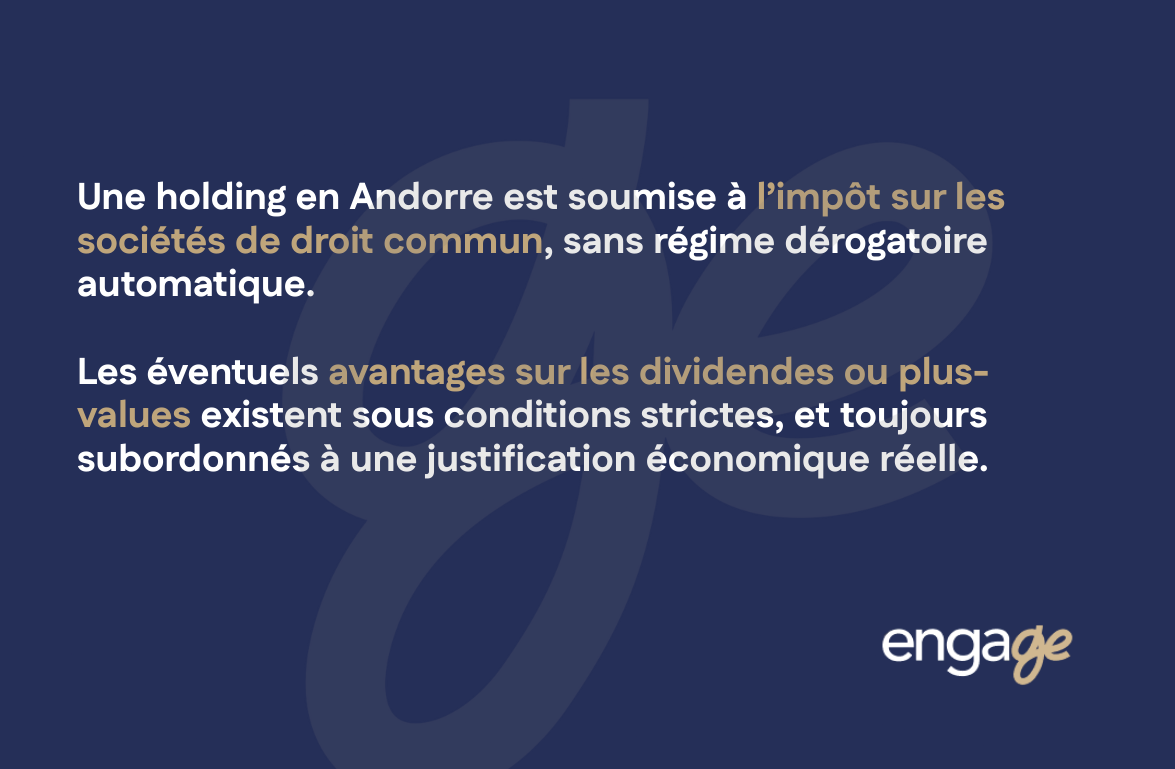

The Andorran holding company is not an "automatic special regime, " but rather a company subject to rules, obligations, and international interpretation.

Your objective must be twofold: to capture potential profits and to secure their enforceability in a cross-border environment.

The corporate tax framework in Andorra is based on a moderate corporate tax rate with stable rules.

The resident holding company is subject to common law, with accounting and reporting requirements and operating rules.

The technical criteria relate in particular to the nature of the holdings, the duration of ownership, and the level of participation.

The modern interpretation adds a cross-cutting requirement: the economic justification of the structure, beyond formal boxes.

The consequence is simple: an isolated tax advantage is never enough if the overall scheme is inconsistent.

The essential conditions can be summarized in three mutually reinforcing pillars.

- The first pillar is substance, with demonstrable premises, organization, governance, and effective decisions.

- The second pillar is economic consistency, as the holding company must have a clear role within the group and in the organization of flows.

- The third pillar is international compliance, as anti-abuse rules and transparency standards extend beyond Andorran law alone.

The necessary vigilance is therefore bilateral: Andorra expects consistency, and the source states scrutinize the reality and usefulness.

Limitations and areas requiring vigilance are often where projects become vulnerable.

Foreign administrations never analyze a holding company "in isolation," but rather in light of conventions, doctrines, and anti-abuse rules.

The risk of contested residence arises when effective management appears to be exercised elsewhere than in the state of incorporation.

The reclassification of cash flows is also possible, particularly if dividends, interest, royalties, or benefits appear artificial.

Exit tax measures or anti-interposition rules can neutralize poorly anticipated schemes.

Coordination with the people who control the structure remains key, as their residence, interests, and decision-making role influence everything.

In addition, certain types of income, such as dividends and capital gains, may be eligible for favorable treatment, but only under certain legal conditions.

Beyond corporate taxation, a key factor concerns the situation of individual shareholders.

When the shareholder is a tax resident in Andorra, the dividends they receive may be exempt from income tax in Andorra, subject to compliance with the applicable conditions.

In practical terms, in this configuration, the distribution of dividends by the holding company does not result in additional taxation at the personal level, which constitutes a significant tax advantage compared to many European countries.

However, this advantage for shareholders cannot be analyzed in isolation.

It requires actual and permanent tax residence in Andorra, as well as a legally and economically defensible holding company.

A formal residence or artificial structure immediately calls this favorable effect into question.

IV. International structuring: cash flows, double taxation, and exit tax

International structuring is not about stacking companies on top of each other, but about organizing defensible flows.

The Andorran holding company is subject to a combination of national rules, agreements, and highly diverse administrative practices.

The main issue is security, because theoretical optimization becomes a cost if it turns into double taxation or litigation.

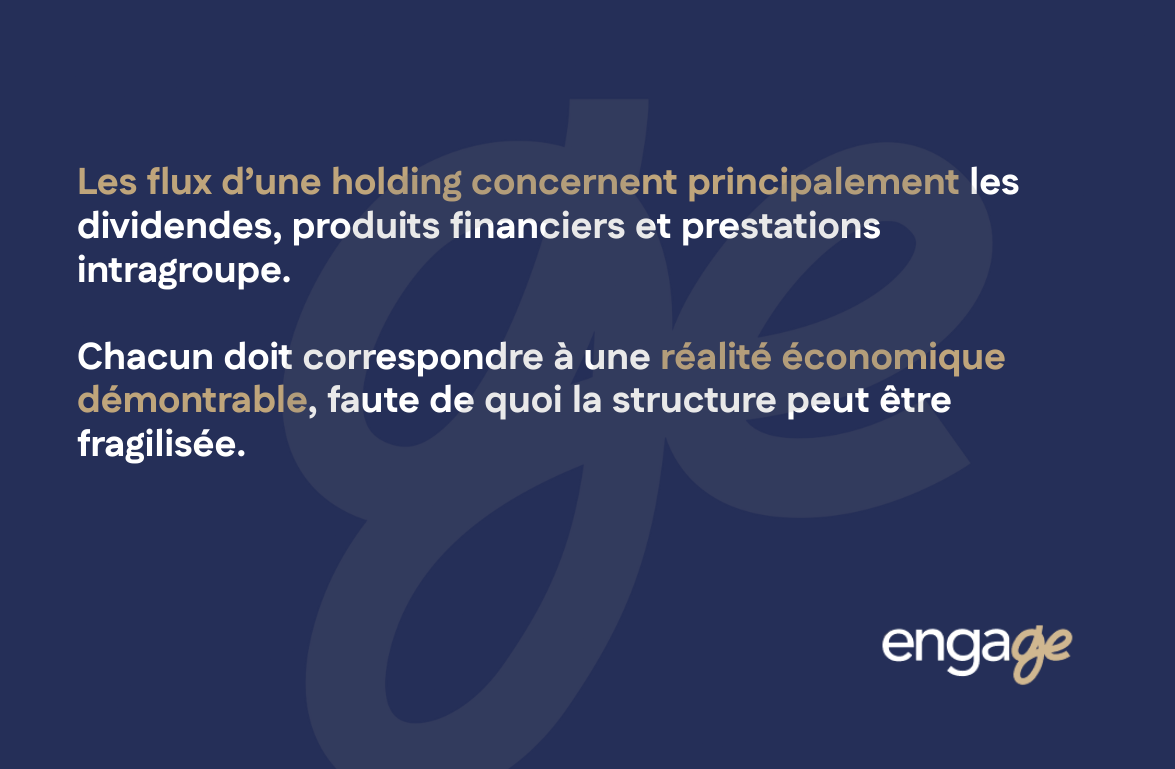

The nature of the flows must be accurately identified, as each category carries its own risks.

Dividends from subsidiaries are often at the heart of the scheme, but they immediately raise the question of withholding taxes.

The financial income received by the holding company may seem neutral, but it must be part of a coherent and well-defined investment strategy.

Intragroup services such as management fees, administrative services, or financial assistance require proof of existence, supporting documents, and a consistent pricing policy.

The typical mistake is the "receptacle" holding company, which collects money without performing any functions, and thus becomes a natural target for criticism.

Documentary discipline thus becomes a tool for protection as well as an internal obligation.

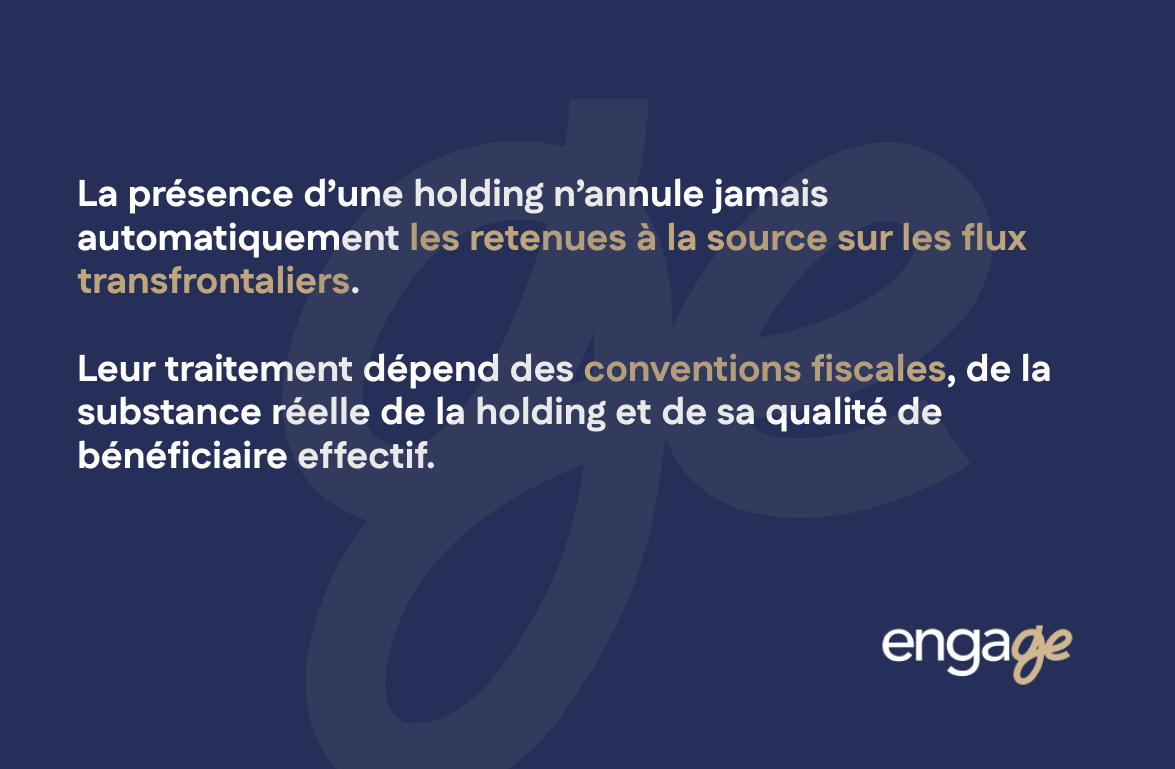

Withholding taxes and double taxation are the most frequent points of contention.

The presence of a holding company never automatically eliminates a withholding tax, as this depends on the domestic law of the source state and the applicable treaty.

The tax treaty may reduce or eliminate certain taxes, but its application is conditional on actual residence and the absence of abuse.

Practical reality requires a "country-by-country" analysis, including the texts themselves, but also the way in which the local administration applies them.

The exit tax is often underestimated because it becomes apparent at the time of the transfer, not at the time of incorporation.

A change of residence by shareholders may trigger taxation on unrealized capital gains, even without a sale.

Internal restructuring can also trigger complex tax mechanisms, particularly when securities or assets are transferred.

The future sale is finally the moment of truth, because the initial structuring choices determine the tax treatment of the exit.

The robust approach consists of viewing the holding company as a tool for trajectory, integrating mobility, transfer, and exit from the outset.

V. Tax residence of executives and shareholders: risk areas

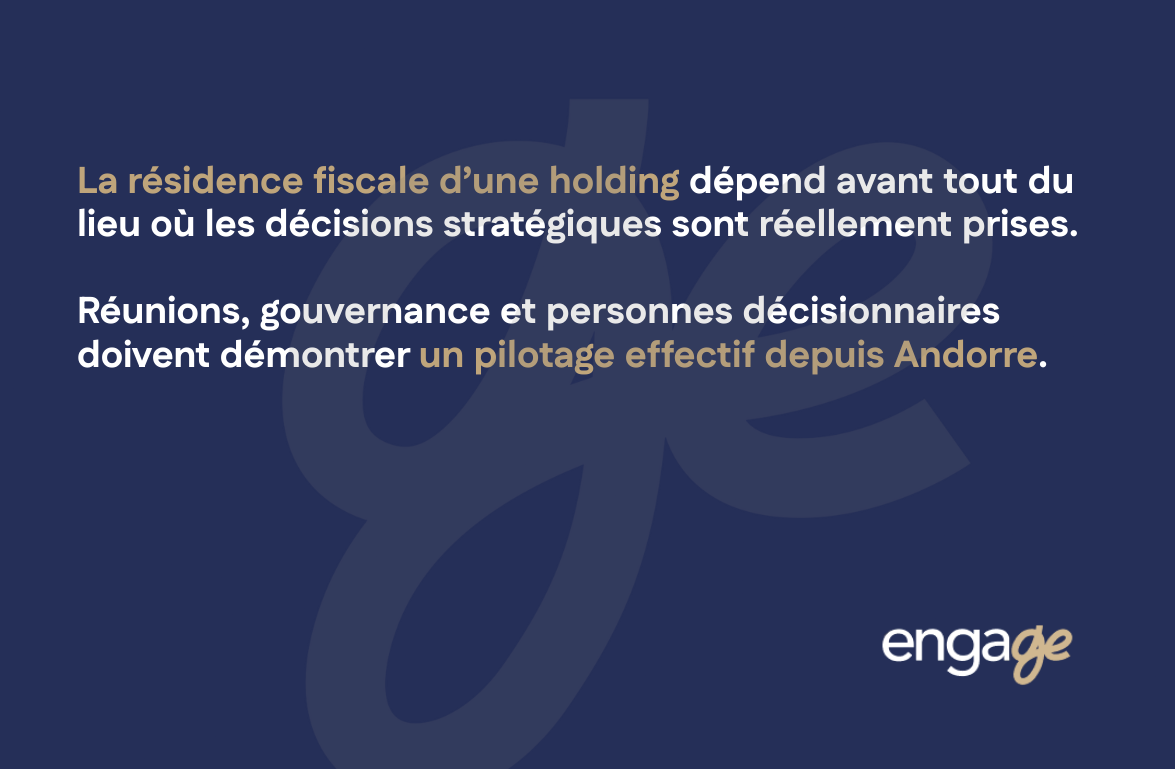

The tax residence of the persons who control the holding company influences the interpretation of the company itself.

The main risk is confusion between the place of incorporation and the place of effective management, as administrations base their reasoning on facts.

Your goal is not to "make people believe," but to build genuine, consistent, and sustainably demonstrable governance.

Effective leadership is demonstrated by concrete and repeatable evidence.

The location where strategic decisions are made is more important than the registered address, because it reveals where the company is actually managed.

The composition of the bodies and the identity of the decision-makers are examined, in particular to detect any concentration of power outside Andorra.

The frequency of meetings and their location are standard indicators, as is the traceability of discussions and decisions.

The risk increases when the same individuals, residing elsewhere, concentrate essential decisions without organizational counterbalances.

The relationship between personal residence and holding companies is particularly sensitive in a cross-border context.

Foreign administrations may consider that the holding company is managed from their territory if the facts point to "remote" management.

Empty governance fuels this analysis, especially if formal bodies do not actually meet, or if decisions are made elsewhere.

The lack of substance further reinforces the doubt, because a holding company without resources or organization resembles an empty shell.

The possible consequence is a reclassification of the place of management, with knock-on tax effects for the company and sometimes for the partners.

Practical security is based on a simple but rigorous architecture.

The definition of powers must be clear, with identified responsibilities and a credible separation between individuals and the company.

Decisions must be documented consistently, because this builds evidence on a daily basis rather than during an inspection.

Consistency in behavior is crucial, because a contradiction between "what is written" and "what is done" weakens the whole.

The best defense remains organized normality: a holding company that functions as a real entity, not as a front.

VI. Tax treaties and international structuring: what you really need to check

Tax treaties are often invoked as a shield, when in fact they are merely a framework.

The key strategy is to understand what they enable, what they condition, and what they do not prevent.

It is in your interest to verify compatibility between cash flow, residence, substance, and anti-abuse clauses before counting on a tax reduction.

The real purpose of a treaty is to avoid double taxation and to allocate the right to tax.

It does not create an autonomous right to optimization, as it always operates in conjunction with the domestic law of the States concerned.

The classification of income determines the applicable article, and incorrect classification can ruin the balance of a scheme.

The resident status of the company invoking the treaty is a transitional issue, and effective management once again becomes central.

Anti-abuse clauses may preclude the contractual benefit even if the formal conditions appear to be met.

The practical limitations are particularly evident in a holding company context.

The substance is analyzed intensively, as administrations want to understand the economic usefulness of the beneficiary entity.

The role of intermediary is the main target, particularly when the holding company appears to be a conduit with no functions or risks of its own.

The consistency of the chain is examined, because an unnecessary step, a superfluous stage, or a break in logic raises suspicion.

A purely textual reading is insufficient, because administrative practice and case law guide the actual application.

Cross-border coordination is becoming a security imperative.

A compartmentalized approach leads to inconsistencies, as each country interprets substance, residence, and beneficial owner according to its own reflexes.

Dialogue between councils allows for the alignment of analyses, the neutralization of contradictions, and the documentation of a coherent economic narrative.

International coherence is therefore not a sum of local solutions, but an overall strategy that is demonstrated in flows and governance.

VII. Shareholder agreements and governance: securing control and strategy

Contractual governance is often what makes the difference between a stable holding company and a fragile one.

Shareholder agreements are not a formality, but a safeguard, as they organize power, liquidity, and conflict prevention.

Your concrete benefit is to transform capital ownership into a clear and predictable decision-making structure.

The strategic role of agreements lies in their ability to supplement statutes where statutes remain general.

The structure of control can be refined, with minority protections and balances tailored to the project.

The decision-making rules become more precise, reducing gray areas and conflicts of interpretation.

The terms and conditions for entry and exit are anticipated, which prevents liquidity crises or blockages when things get tense.

The holding company gains predictability, which is essential for long-term wealth management or entrepreneurial planning.

Structural clauses should be thought of as mechanisms for stability, not as traps.

Preemptions protect shareholders by controlling transfers.

Inalienability can provide security in the early years, provided that it is proportionate and consistent with the holding period.

Liquidity mechanisms organize exits, reduce conflict, and provide economic visibility to partners.

Strategic decisions can be locked in by reinforced majorities to preserve the project's DNA.

The adjustment to the type of holding company is crucial, because a family holding company is not governed in the same way as a holding company with investors.

Family agreements and investor agreements respond to almost opposite rationales.

The family pact aims to achieve stability, continuity, and conflict prevention through clear and accepted rules.

The investor agreement focuses on liquidity, protection of financial rights, and exit scenarios that are defined from the outset.

Consistency with the articles of association must be perfect, as any contradiction between the two texts could weaken the structure at the worst possible moment.

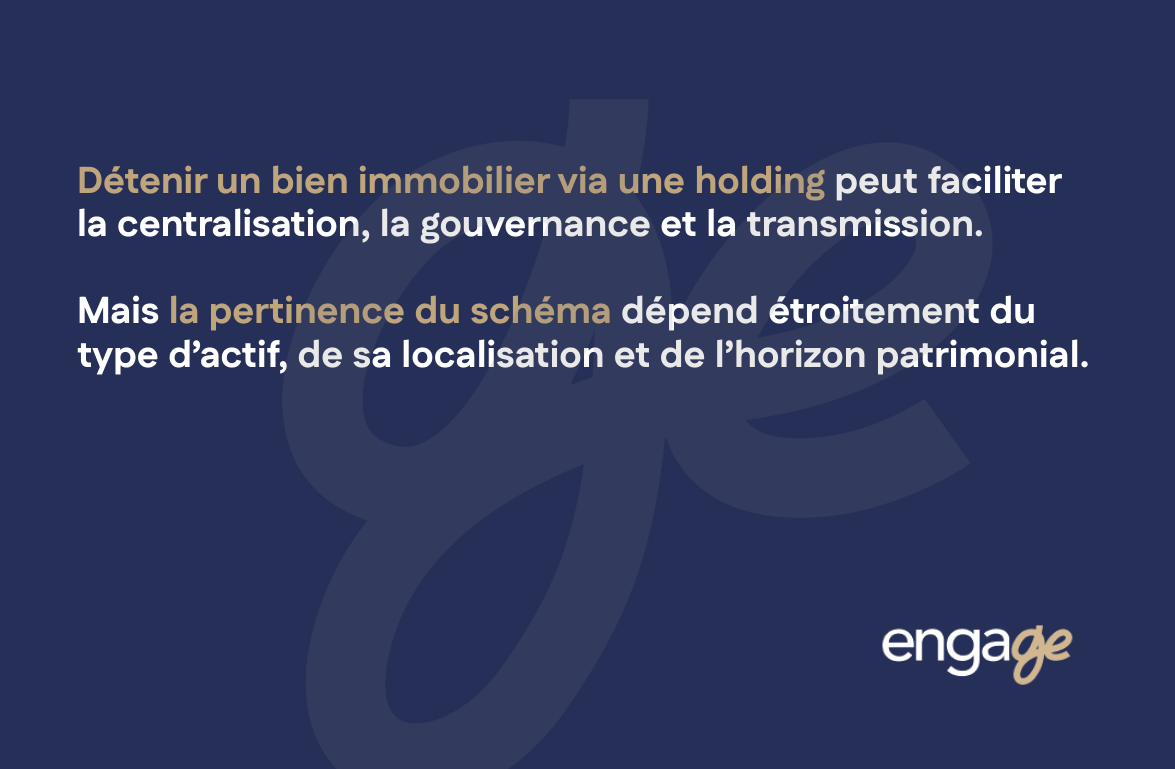

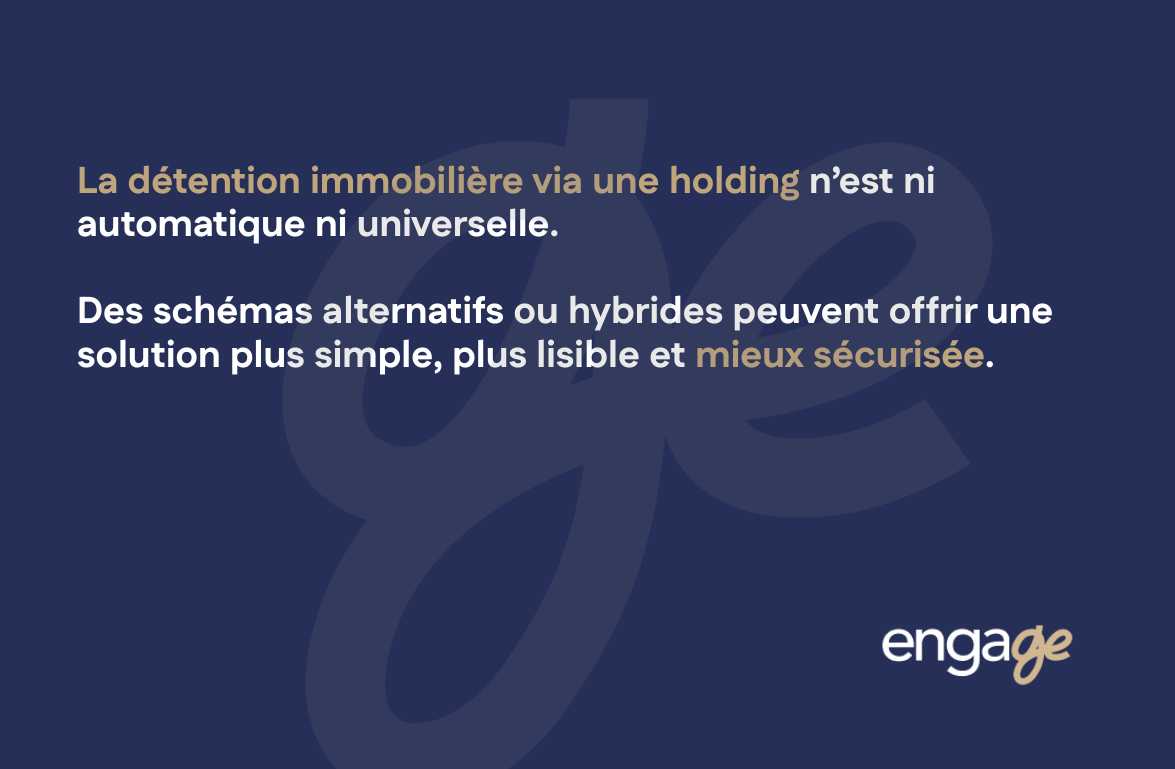

VIII. Real estate: opportunity or false good idea?

Real estate is often the asset that people want to "put in a holding company" because it is reassuring and carries weight.

The reality is more nuanced, as real estate is always subject to the tax and legal systems of the country where the property is located.

Your challenge is to avoid false elegance: a structure that looks good on paper but is costly and questionable in practice.

The apparent logic of holding via a holding company is understandable.

Centralization provides a consolidated view and can simplify certain decisions.

Transferring ownership via securities may seem simpler than transferring the property directly, particularly for a gradual family strategy.

Family governance can also be clarified, with decision-making rules and intergenerational planning.

Risk separation may be sought, especially if certain assets are to be isolated.

The immediate limitation is that these advantages are often legal, whereas the constraints are often fiscal and operational.

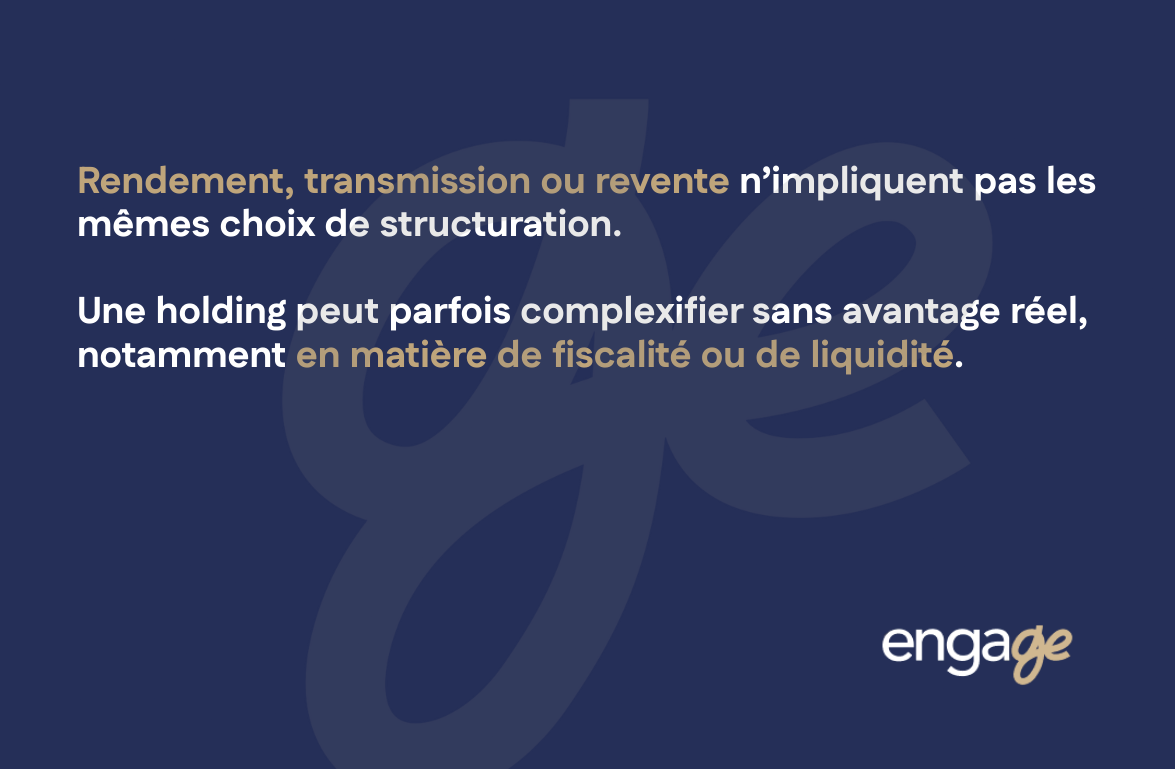

The analysis by objective must therefore guide the decision.

In terms of return and long-term ownership, the holding company may add costs and obligations without improving the net return.

In terms of transmission, it can help, but it must be weighed against local mutation rules and the classification of companies as predominantly real estate-based.

In terms of resale, it does not guarantee neutrality or ease, as some jurisdictions treat the transfer of securities as an indirect real estate transfer.

The correct approach is to compare the actual effects country by country, rather than applying a standard model.

Methodological caution is often the best strategy.

The superimposition of levels can reduce readability, complicate financing, and give rise to anti-abuse interpretations.

Separate structures may sometimes be more appropriate depending on the nature of the asset and the objective pursued.

Hybrid schemes may also be considered, but only if overall consistency can be demonstrated.

The basic rule remains to choose the most defensible structure, not the most sophisticated one.

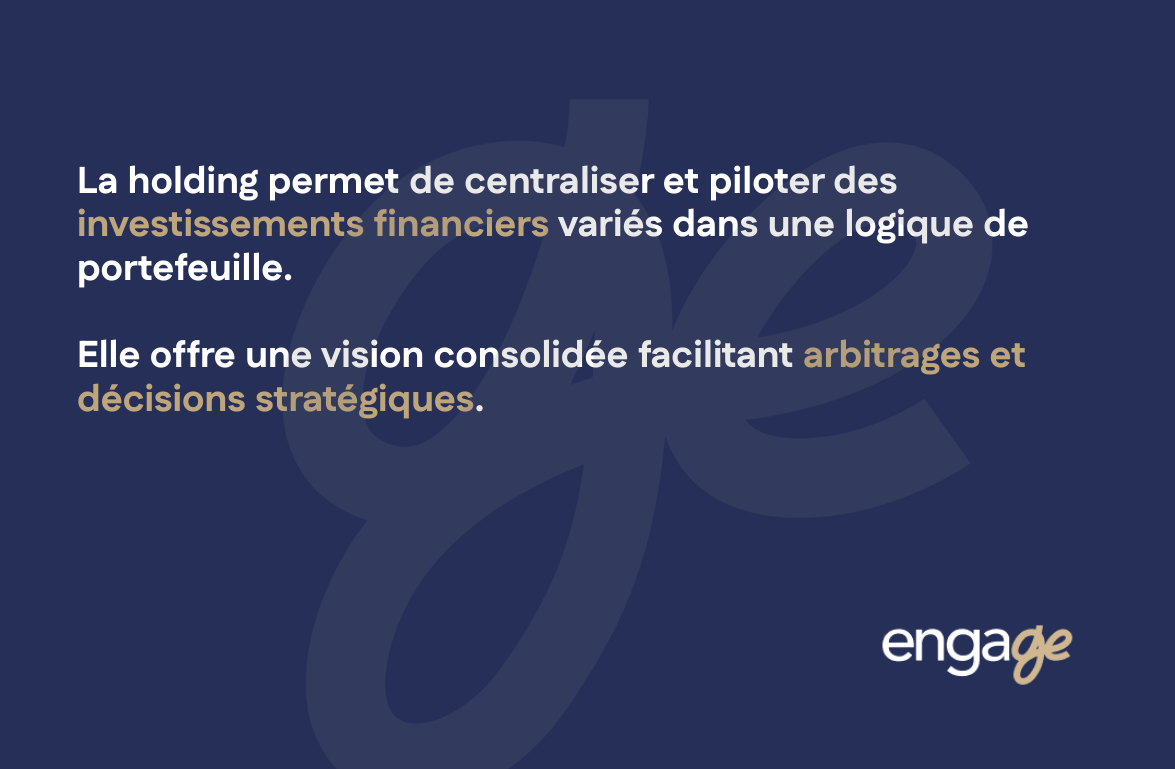

IX. Andorran holding companies and international financial investments

Financial investment via a holding company may be appropriate, but it requires discipline, as banks and government agencies want to understand "why" and "how."

The investment holding company should resemble a management entity, not a simple intermediary account.

Your advantage is centralization, but your obligation is consistency and traceability.

Centralizing assets provides portfolio visibility and facilitates arbitrage.

Investments in listed or unlisted equities can be grouped together to manage risk and strategy.

Investment funds can be held in a unified framework, which sometimes simplifies asset governance.

Cash products can also be organized, but they must be compatible with the purpose of the structure.

A consolidated vision improves decision-making, but it should not obscure the need for a formalized strategy.

Investment discipline is at the heart of defensibility.

A written policy clarifies asset classes, objectives, and the arbitrage framework.

The traceability of decisions provides protection because it shows that choices are not opportunistic but structured.

The consistency of flows must be constant, as inconsistent movements fuel suspicions of artificial manipulation.

The main risk is that the holding company will be perceived as a shell company, with no logic of its own and no real governance.

Banking compliance is a reality check, often more demanding than anticipated.

The documentation must be legible, including articles of association, organizational charts, governance, and economic justification.

The identification of decision-makers and powers must be immediate, because the bank wants to understand who controls and who decides.

The traceability of the origin of funds is essential, and any gray areas can block or weaken the banking relationship.

The practical consequence is that governance and compliance are not incidental, but operational.

X. Family asset organization: governance and control

The family holding company shows its true value when it organizes powers, not just assets.

The central issue is stability over time, because the major risk to wealth is often conflict, not taxation.

Your goal is to build a framework that will survive changes in generations, moods, and trajectories.

Structuring power makes it possible to separate economic ownership from decision-making.

The separation of roles facilitates the gradual integration of subsequent generations without upsetting the balance of the strategy.

Evolving governance allows for the adjustment of voting rights, decision-making powers, and control mechanisms.

Strategic continuity is better preserved because decision-making centers remain identified and organized.

Preventing conflicts involves making explicit topics that we sometimes prefer to avoid.

The absence of rules creates tension, as everyone projects their expectations onto a silent structure.

Formalizing rights and obligations provides a framework, reduces interpretations, and facilitates arbitration.

The decision-making procedures must be clear, particularly with regard to structural decisions and majority thresholds.

Exit mechanisms must be anticipated, as it is often the exit that triggers the crisis.

Asset stability depends as much on technique as on adherence.

Consistent rules are useless if they are not understood and accepted by those concerned.

A holding company becomes useful when it pacifies and organizes, rather than adding a layer of complexity without real governance.

XI. Transmission, protection, and liquidity

Transmission is not an event, but a process.

The holding company can be a catalyst for this, provided that taxation, inheritance law, governance, and family realism are taken into account.

Your challenge is to create an organization that allows you to give, protect, and plan for the exit without compromising consistency.

Anticipating transfer by securities often allows for a more gradual approach.

Donations of securities can be structured, phased, and adapted to changing personal circumstances.

The separation of economic and power interests makes it possible to transfer value without immediately losing control, provided that governance is properly structured.

Tax planning remains essential, as the rules applicable at the time of transfer determine the security of the arrangement.

Protecting spouses and heirs requires coordination with applicable inheritance law.

The holding company alone does not protect anything if it contradicts civil or international inheritance rules.

The protective strategy involves aligning ownership, powers, and actual family objectives.

Overall consistency is therefore key, because an isolated structure becomes vulnerable at the very moment when it should be providing protection.

Liquidity must be considered from the outset, because life does not always follow the financial plan.

A partial sale may be necessary to reallocate, finance, or adapt a strategy.

The departure of a partner must be possible without drama, thanks to pre-established rules and buyback or transfer mechanisms.

Gradual divestment must be a viable option, particularly when a transfer or change in life cycle is approaching.

The robust holding company offers options rather than freezing assets.

XII. Decision methodology: when to create (or not to create)

The decisive question is not "is it attractive," but "is it relevant and defensible."

A holding company is a structural tool, and a tool is only good if it is suited to the job at hand.

Your method must therefore filter opportunities based on consistency, potential substance, and international trajectory.

Adapted cases share repetitive characteristics.

An international dimension often makes it useful to centralize detention and governance.

A diversified portfolio may justify a steering committee, especially if decisions are frequent and structured.

A long-term outlook increases interest, as the holding company gains value over time.

A commitment to formalized governance is a positive sign, as it increases transparency and security.

Risky situations must be identified without complacency.

The impossibility of substance mechanically weakens the holding company, because it then becomes a form without reality.

An exclusively fiscal objective is open to challenge, as opportunistic schemes are the most vulnerable to attack.

An overly simple structure may not justify the added complexity, and the recurring cost then becomes a penalty.

Uncontrolled international constraints create inconsistencies, and inconsistency is the best ally of requalifications.

The strategic checklist is used to make decisions, not to reassure oneself.

Clarifying objectives is the first step, because a tool without a purpose becomes a complication.

Analyzing the residence of executives and shareholders is essential, as it influences international perception.

Mapping the location of assets allows you to anticipate restrictions, agreements, and administrative practices.

Defining the horizon for transfer, retention, or disposal allows you to choose a plan that is compatible with the trajectory.

Testing sustainable governance means asking yourself whether you will be able to maintain discipline over time, not just sign the articles of association.

XIII. Implementation: stages, costs, long-term discipline

Creating a holding company is a starting point, not an end point.

The value of the schema depends on its ability to function, remain consistent, and adapt to changes.

Your main risk is to build a perfect structure at T0, then let it drift due to a lack of discipline.

The initial structuring begins with the choice of the legal form best suited to the type of partners and the objective.

The corporate purpose must be balanced, because if it is too narrow, it hinders development, and if it is too broad, it undermines clarity.

Governance must be considered from the outset, with powers, decision-making rules, and control mechanisms aligned with reality.

The banking relationship must be anticipated, as it requires transparency, documentation, and overall consistency.

Recurring costs must be included in the actual profitability of the scheme.

Accounting costs are incompressible, particularly in relation to record keeping, financial statements, and reporting obligations.

Legal costs exist over time, as a living holding company requires adjustments, decisions, and formalization.

Administrative obligations require method and rigor, as deadlines and formalities structure compliance.

Compliance requirements are increasing, making governance a security issue, not an option.

The right question, then, is whether the expected benefit justifies these costs in a proportionate manner.

Long-term discipline is the real key to success.

The regulatory environment is changing, and a holding company must be able to adapt without losing sight of its core purpose.

Functional consistency must be maintained, as the gradual drift toward inactivity renders the scheme questionable.

Real governance must remain alive, documented, and aligned, because it is what protects against anti-abuse interpretations.

Conclusion: a patrimonial decision before a fiscal one

Setting up a holding company in Andorra is neither a universal solution nor an automatic recipe fortax optimization.

It does not follow a logic of standardization.

It is a demanding tool that requires careful consideration beforehand and a thorough understanding of heritage issues.

It is aimed at mature, already structured estates that have reached a stage where the issue is no longer one of accumulation, but of organization and sustainability.

When approached methodically, rigorously, and consistently, its effects are nevertheless significant.

It reduces tax erosion over time, without resorting to fragile or questionable mechanisms.

It secures governance by clarifying roles, powers, and balances.

It helps simplify estate planning by restoring clarity to structures that have become complex over time.

But its essential contribution lies elsewhere.

It allows you to regain true freedom of choice.

The freedom to make decisions without incurring a systematic penalty.

The freedom to transmit without abrupt interruption.

Finally, the freedom to manage your assets as a separate project, aligned with a new stage in your life.

Are you considering setting up a holding company in Andorra or optimizing an existing structure?

Each financial and business situation requires a specific analysis, taking into account your objectives, constraints, and international environment.

We invite you to contact us to initiate a confidential and structured discussion.

This initial analysis allows you to make confident decisions and lay the foundations for a coherent, sustainable, and defensible structure.