Andorra tax advice: understanding, anticipating and securing your wealth strategy

Introduction

In an increasingly complex European tax environment, the search for stability and clarity has become a priority for managers, investors and business leaders.

Increased tax pressure, tighter controls, shifting finance laws and legal instability fuel a feeling of uncertainty.

For many high-net-worth taxpayers, this situation calls for strategic thinking: how to structure their wealth, protect their assets, and optimize their tax situation within a legal, transparent, and compliant framework?

It is in this context that Andorra stands out as a credible tax and wealth management alternative that is modern, stable, and compliant with the international transparency standards set by the OECD. Located between France and Spain, the Principality has successfully transformed its image: once perceived as a tax haven, it is now recognized as a fiscally competitive but legally demanding jurisdiction.

With an income tax rate capped at 10%, a corporate tax rate of 10%, and no wealth tax, inheritance tax, or confiscatory property tax, Andorra offers an attractive environment while complying with European rules on international taxation, information exchange, and the fight against tax fraud.

However, taking advantage of this favorable tax regime cannot be improvised. Each situation requires a personalized analysis of assets, a detailed understanding of international tax law, and rigorous support from a tax advisor, tax lawyer, or accountant who is well versed in Franco-Andorran tax practices.

ENGAGE assists taxpayers, executives, and investors with this process: tax audits, structuring of holding companies, management of capital gains on securities and real estate, income tax returns, compliance with administrative obligations, and monitoring in the event of tax disputes or adjustment procedures.

The goal is not to evade taxes, but to understand them, master them, and turn them into a strategic lever.

Click here to book a strategic meeting with an ENGAGE consultant and find out how to turn your Andorran tax situation into a truly sustainable wealth strategy.

I. The European tax context: between instability and the search for sustainable solutions

1. Constantly rising tax pressure

For more than a decade, the European tax landscape has been undergoing a profound transformation.

Economic competitiveness, the fight against public deficits and the quest for additional tax revenues have led Member States to strengthen their tax and control systems.

As a result, European taxpayers—both individuals and businesses—now bear one of the highest tax burdens in the world.

In France, this trend is reaching a critical level.

Income tax is now levied on a progressive scale , with the top bracket exceeding 45%, not including social security contributions (CSG, CRDS) which add to the overall burden.

The real estate wealth tax (IFI), which replaced the ISF, maintains high taxation on real estate assets held by wealthy households, without distinguishing between productive and patrimonial assets.

Added to this are the property tax, CFE (cotisation foncière des entreprises), CET (contribution économique territoriale) and dividend tax - all levies that directly affect the profitability of investments and the development capacity of companies.

Even tax credit and tax reduction schemes such as Pinel, Girardin and Crédit d'Impôt Recherche (CIR) no longer compensate for the intensity of the overall drain.

For companies, the situation is just as restrictive.

Although the corporate income tax (CIT) rate has fallen slightly in recent years, it remains high in comparison with neighboring jurisdictions.

Sole proprietorships and self-employed professionals subject to the actual tax regime or the industrial and commercial profits (BIC) regime must also contend with a complex system, where the deductibility of expenses and the depreciation of fixed assets require a detailed understanding of tax matters.

In this environment, the tax authorities—or more precisely, the tax administration—have extensive powers: document checks, accounting audits, adversarial adjustment procedures, and even tax reassessments accompanied by penalties. The annual finance law, which is often unstable, constantly changes the rules of the game, further complicating the predictability of tax outcomes for taxpayers.

Beyond national taxation, cooperation between administrations has reached an unprecedented level.

Under the impetus of the OECD and the European Commission, member countries are now participating in the automatic exchange of banking information (CRS standard) and the implementation of BEPS (Base Erosion and Profit Shifting) standards.

These measures are designed to prevent tax evasion and harmonize international tax rules, but they also lead to increased monitoring of cross-border flows, transfer pricing, and offshore holding structures.

As a result, business leaders and international investors now have to navigate a complex and ever-changing set of rules, where every decision—whether it involves a donation, a dividend transfer, a change of tax residence, or a corporate restructuring—can have significant tax implications.

For non-residents or expatriate taxpayers, the risk of tax domicile requalification is particularly sensitive.

The French tax authorities, particularly Bercy, apply a broad interpretation of tax domicile : a simple center of economic interests (income, investments, professional activity or real estate in France) is often enough to maintain French tax liability, even if you move abroad.

Tax adjustment or recovery procedures can then extend over several years, with interest on arrears and substantial financial penalties.

This situation places high-income taxpayers and large companies in a delicate position: how can they secure their tax strategy, reduce the risk of reassessment, and maintain full compliance with national and international legislation without compromising the performance of their assets?

It is at this intersection between wealth strategy, tax law, and international management that the need for professional support from a tax specialist, accountant, or tax lawyer arises. Their role is to provide a clear understanding of the scope of taxation, identify opportunities for deductions, exemptions, or legal tax breaks, and anticipate the effects of local and international taxation on the taxpayer's overall wealth.

In such a context, the search for a stable, transparent and predictable tax framework becomes a strategic imperative.

And that's precisely what Andorra offers, with its modern, competitive tax system attracting a growing number of entrepreneurs, executives and wealthy families every year looking to combine legality, security and optimization.

2. Andorra: a legal, structured alternative

At a time when taxation is becoming a strategic component in its own right for companies and individuals alike, the search for a stable, predictable tax framework has become a genuine asset sovereignty issue.

Faced with growing public deficits, Europe's major powers are multiplying tax hikes and successive reforms, often passed without any long-term vision.

This instability creates permanent legal uncertainty, slowing down investment, complicating the transfer of ownership and discouraging initiative.

Andorra has emerged as a legal, transparent and controlled alternative.

In just a few years, the Principality has carried out an in-depth reform of its tax system, abandoning any logic of opacity in favor of a model in line with international standards, while preserving its competitiveness.

Today, Andorra's tax system is recognized as one of the most modern in Europe.

Itcombines low tax rates, regulatory stability, simplicity of management, and a high degree of legal certainty for taxpayers, whether residents, non-residents or company directors.

A tax model based on clarity and proportionality

Andorra applies a principle of tax proportionality: each taxpayer contributes to public funding according to his or her actual income, without excess or distortion.

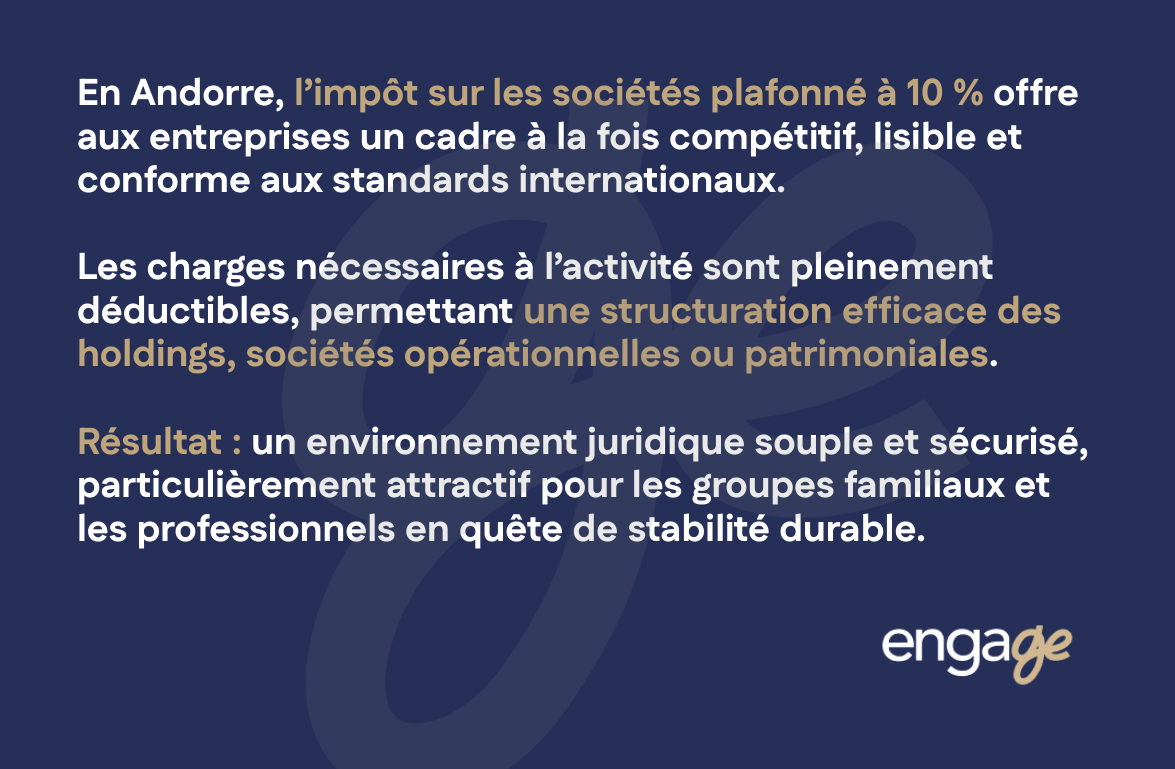

The maximum income tax rate is set at 10%, irrespective of the category of taxable income (earned income, dividends, professional profits, income from movable property or property).

By way of comparison, this rate is over 70% lower than that applicable in most European Union countries.

Personal income tax (IRPF) is calculated on a simple, predictable basis:

- Professional income and industrial and commercial profits (BIC) are taxed after deduction of professional expenses and allowable depreciation.

- Income from movable property (interest, dividends, capital gains) may, under certain conditions, be exempt when it comes from an Andorran company or qualified foreign investment.

- Real estate income is treated favorably, with the possibility of deducting actual expenses related to the management, maintenance, and improvement of the property.

In practice, this gives Andorran taxpayers rare visibility over their taxable income. This transparency, combined with a capped direct tax rate, enables optimum management of taxable income and precise control of the effective tax rate.

In addition, there is no wealth tax, social security contributions or CSG to add to personal taxation.

Inheritance and gift taxes are non-existent, making it possible to pass on or restructure family assets without confiscatory taxation.

A competitive, incentive-based corporate tax system

Andorran business taxation is based on a similar principle of simplicity and competitiveness.

Corporate income tax (CIT), at a single rate of 10%, applies to taxable income after deduction of business expenses: salaries, rent, depreciation, loan interest, management fees, and professional expenses.

In this way, holding companies, real estate companies and family asset structures can be organized within a solid, compliant legal framework.

Andorran company law, inspired by European models, allows for great flexibility in governance, capital distribution, and shareholder protection.

This tax and legal model is particularly attractive to family groups and self-employed professionals seeking to consolidate their activities in a neutral jurisdiction, while remaining fully compliant with international conventions.

Streamlined, rational VAT (IGI)

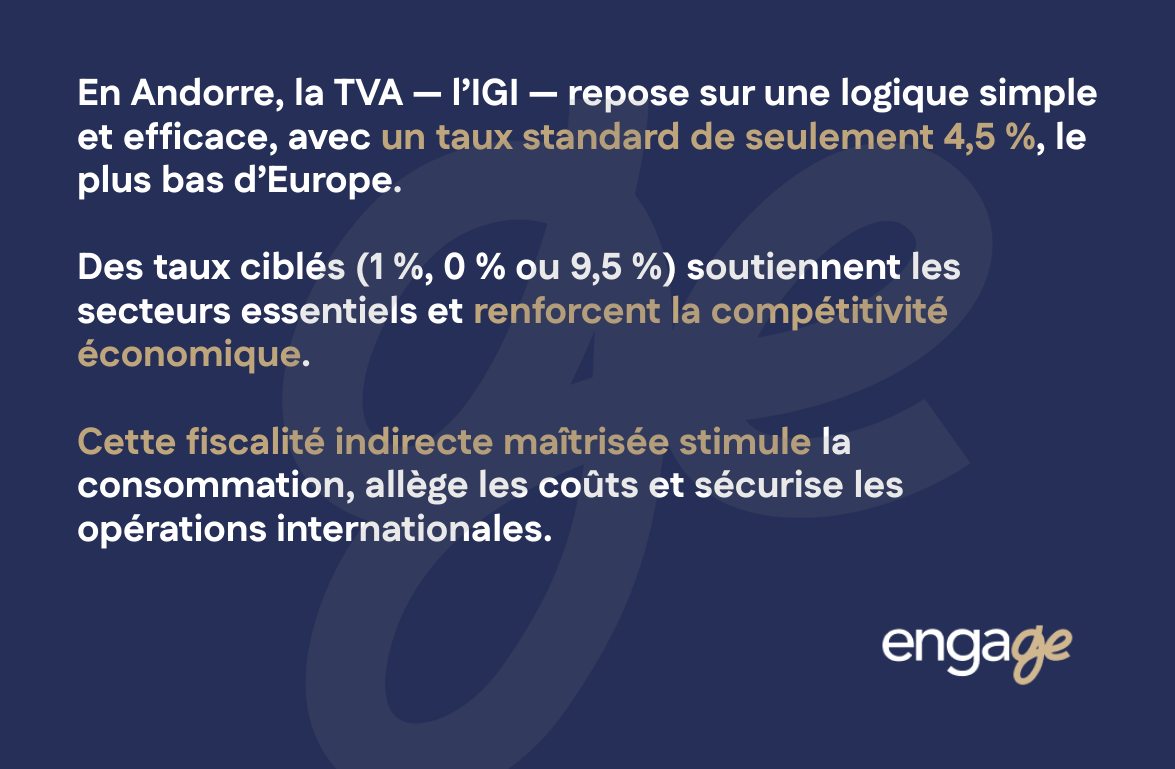

Andorra applies a value-added tax called Impost General Indirecte (IGI).

Its standard rate of 4.5% is the lowest in Europe, and certain sectors benefit from reduced rates:

- 1% for basic foodstuffs,

- 0% for educational, medical or social activities,

- 9.5% for financial and banking services, subject to a specific regime.

This balanced indirect tax system has a virtuous circle: it stimulates domestic consumption, boosts the competitiveness of local businesses, and helps control production costs.

For international services, VAT may often be deductible or not applicable, depending on the place of taxation determined by double taxation agreements.

A protective asset framework conducive to inheritance

One of Andorra's major assets is its wealth tax system.

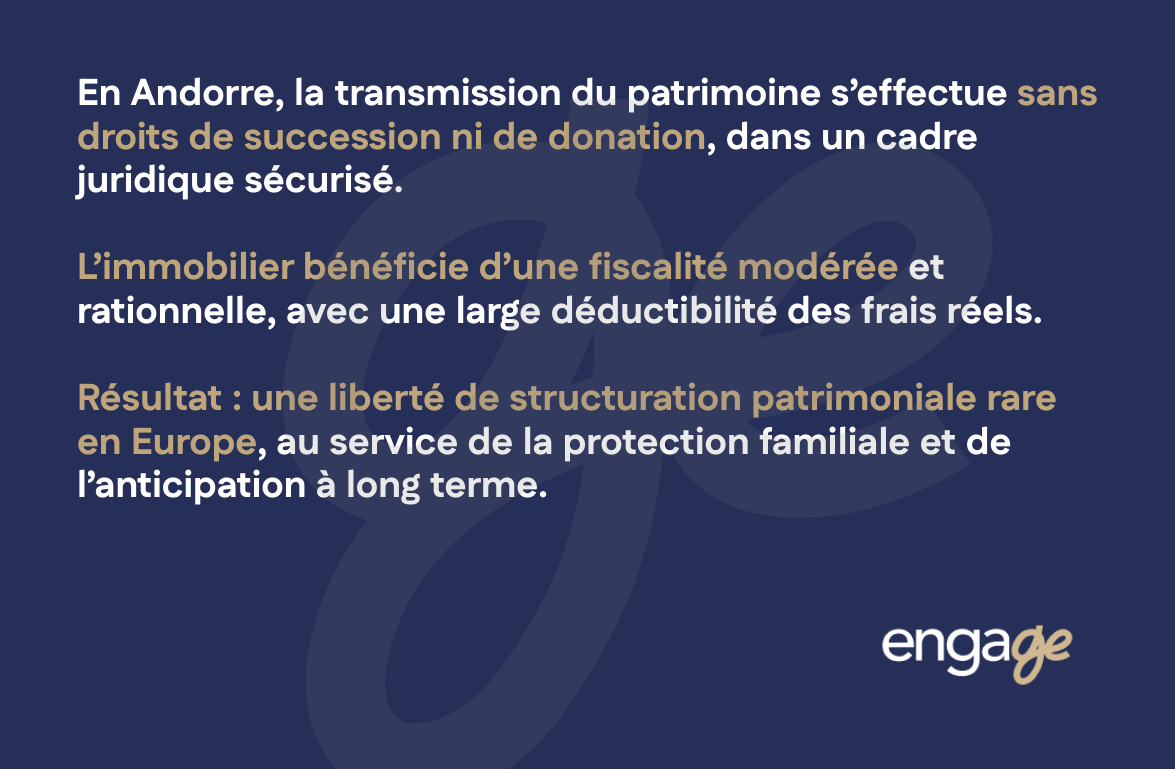

Gifts, inheritances and capital gains on real estate are treated exceptionally favorably.

- There are no inheritance or gift taxes. Transfers between parents and children, spouses or partners are tax-free.

- Rental income from real estate in Andorra is subject to moderate taxation, with the possibility of deducting actual costs (insurance, work, management, loan interest).

- Foreign investors can acquire real estate either personally or through a company in order to optimize the ownership, management, and transfer of their assets.

This coherent approach to wealth management offers a freedom of structuring that is rare in Europe, combining legal flexibility with tax efficiency.

Transparent, recognized tax compliance

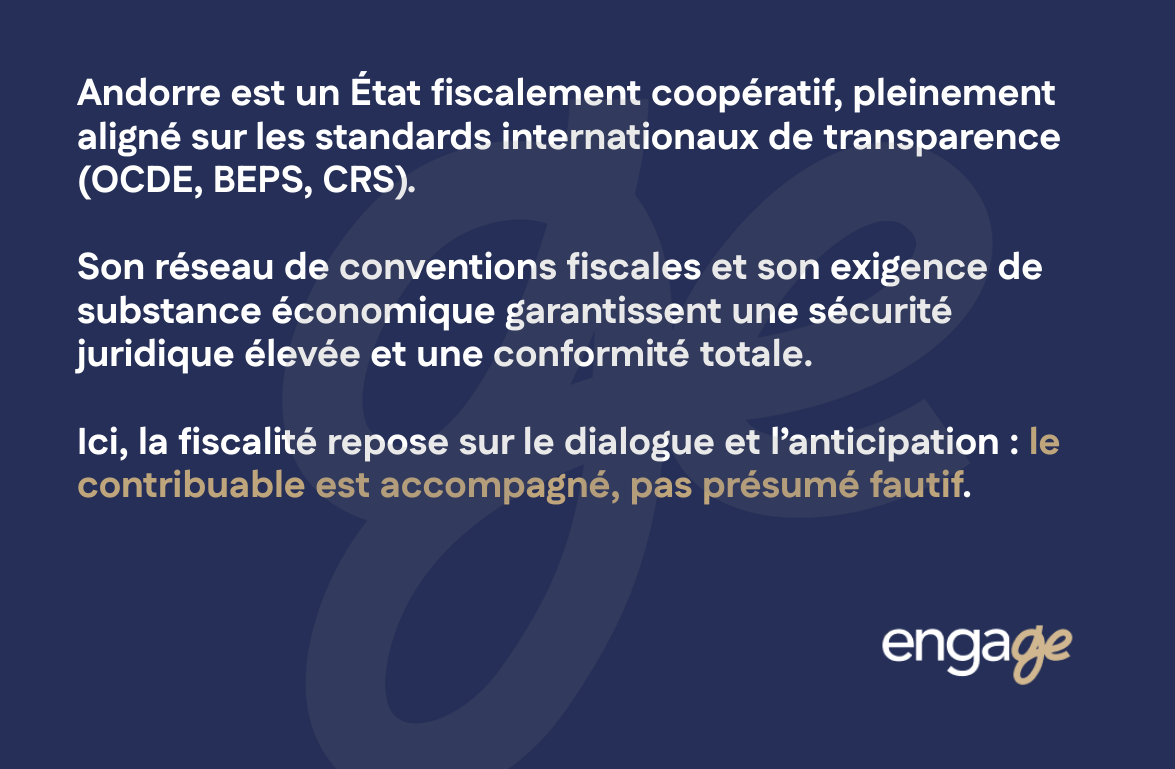

Contrary to popular belief, Andorra is not a "tax haven", but a cooperative state that fully respects the principles of international transparency.

The Principality has signed bilateral tax treaties with France, Spain, Portugal, Luxembourg and several other countries, to avoid double taxation and guarantee legal certainty for taxpayers.

These agreements provide a framework for tax residency, dividend flows, capital gains, and clarify the jurisdiction of each administration.

Andorra also applies the OECD's BEPS standards and participates in the automatic exchange of tax information (CRS standard), reinforcing its legitimacy with the European authorities.

It has implemented legislation on economic substance, requiring companies established within its territory to have a genuine presence.

Andorra's tax authorities are known for their pragmatic approach: they give priority to prevention, dialogue and upstream reassurance through tax rescripts or prior opinions.

Taxpayers can therefore consult the authorities before undertaking any sensitive transactions, thereby ensuring compliance and avoiding the risk of disputes.

This cooperative governance creates a unique climate of institutional trust: the taxpayer is considered a partner, not a suspect.

A tax system serving a sustainable economic vision

Finally, the Andorran model is based on a clear philosophy: to make taxation a tool for economic development, not a constraint.

By encouraging business start-ups, foreign investment and talent mobility, the Principality attracts a population of entrepreneurs and investors keen to combine performance, ethics and compliance.

The Andorran tax system is not designed to evade taxes, but to reward transparency and good management.

It's a model of balanced taxation, where low rates go hand in hand with rigorous administration and constant cooperation with international authorities.

For business owners and wealthy families, Andorra represents a rare opportunity: the chance to carry out their activities or structure their assets in a clear, respected and predictable tax environment, where entrepreneurial freedom finally finds its meaning.

II. Taxation as an asset strategy tool

1. From simple domiciliation to global structuring

Choosing Andorra to optimize your tax situation is not a matter of "moving your address".

It's a comprehensive wealth management project, involving the individual, the company and the family in a process of thoughtful, compliant and sustainable structuring.

The well-informed taxpayer does not seek to evade taxes, but to anticipate, rationalize and control them.

In an unstable and sometimes hostile European tax environment, this structured approach becomes a form of wealth governance in its own right.

With this in mind, Andorra's tax system is not an end in itself, but a means to an end.

A way to restore consistency to the management of global assets: real estate, financial portfolios, industrial holdings, corporate income, dividends or intra-group flows.

A way of preserving the economic performance of companies and ensuring family and professional continuity.

And finally, a way to ensure that every financial or legal decision is based on solid, transparent, and recognized foundations.

The support of a tax advisor or a wealth management consultancy like ENGAGE is therefore crucial.

His role is not limited to simply filing tax returns: it involves designing a tailor-made tax structure in which each element—structure, residence, cash flow, company, assets—is consistent and aligned with the legal requirements of the jurisdictions concerned.

ENGAGE provides its customers with comprehensive asset engineering services that include :

- the creation of holding companies to isolate risks and facilitate the transfer of assets;

- structuring operating companies for managers wishing to benefit from a 10% corporate tax rate, while protecting their personal assets;

- coordination between dividend, fee, and capital gains flows inorder to avoid double taxation and benefit from international tax treaties.

Each configuration is analyzed in the light of comparative tax law (France, Spain, Luxembourg, Andorra) and company law.

The final scheme is legally secure, compliant with OECD standards, and validated from an accounting and tax perspective.

This methodical approach distinguishes ENGAGE from a conventional firm: the aim is not to propose an arrangement, but to build a coherent and compliant wealth strategy, capable of standing the test of time and a possible cross-border tax audit.

2. Tax residence : the cornerstone of wealth management strategy

Tax residency is the cornerstone of any international wealth structuring strategy.

It determines the country of taxation, the regime applicable to income and capital gains, and all the related reporting and compliance obligations.

It also influences heritage protection, international mobility and intergenerational transmission.

In a context marked by the automatic exchange of information and the strengthening of tax cooperation between countries, securing one's tax residence has become an essential prerequisite for any asset optimization.

In Andorra, this setting is particularly attractive.

Andorran domestic law is based on simple, clear and stable criteria, guaranteeing both legal certainty and tax predictability. This stability, combined with a competitive tax regime, explains why the Principality has become a destination of choice for many managers, investors and wealthy families.

The criteria for Andorran tax residence

Andorran law is distinguished by its clarity: to be considered a tax resident in Andorra, it is sufficient to meet one of the following two legal conditions:

- Staying in Andorra for more than 183 days per year.

Occasional and short-term absences do not affect tax residency status as long as the center of life remains in Andorra.

- Establish your center of economic interests there.

This criterion is based on the location of income and assets.

When a person receives the majority of their income from Andorra or transfers their economic assets there, they may be considered an Andorran tax resident, even if they do not meet the threshold of 183 days of annual presence.

Compliance with just one of these conditions is sufficient to qualify as an Andorran tax resident.

In practice, expatriate candidates often do not initially have their business center in Andorra.

Legal solutions exist to organize this transfer, notably through the creation of an Andorran holding company, the centralization of asset income or the domiciliation of strategic activities.

Tax treaties and loss of original residence

Obtaining Andorran tax residency alone is not enough to secure international mobility.

To avoid double taxation, it is necessary to terminate the original tax residence and, where applicable, resolve any conflicts of residence by applying tax treaties.

According to each double taxation treaty with the country of departure - as is the case with France - the conflict of residence is decided according to a hierarchy of criteria:

- Permanent home

- Center of vital interests (economic and family)

- Usual place of residence

- Nationality (subsidiary criterion)

In the absence of a tax treaty, the loss of original tax residence must be organized in accordance with the domestic law of the country of departure, which requires a personalized and rigorous analysis.

Such an operation requires combined expertise in Andorran tax law and international taxation.

This means coordinating strategy with tax specialists who are familiar with the legislation of the country of origin, to avoid any risk of reclassification by foreign tax authorities.

Proof of tax residence : a strategic issue

Legal texts alone are not enough to secure a tax residence.

It's the facts that take precedence during an inspection.

Tax authorities examine the concrete reality of the situation: place of habitual residence, economic and family center, consistency between declared residence and actual residence.

Solid documentation is therefore the best protection.

ENGAGE supports its customers in this strategic dimension by ensuring :

- the creation of a complete and traceable residence file (leases, invoices, local subscriptions, bank documents, proof of physical presence, memberships, etc.);

- anticipating the specific concerns of foreign tax authorities, particularly French ones;

- guaranteeing overall consistency between assets, actual presence and declared residence.

This structured approach provides a solid defense in the event of a tax audit or cross-border dispute.

A strategy to suit every asset profile

Tax residency requirements differ considerably depending on the taxpayer's profile.

A company director will not have the same constraints as a financial investor, an international artist or an annuitant.

Each situation requires a tailor-made combination of tax residence, asset structuring, and income strategy.

ENGAGE develops solutions adapted to each profile, integrating :

- legal and tax structuring of assets,

- international mobility and territoriality rules,

- securing financial flows ,

- and estate planning.

The aim is to guarantee both legally compliant tax optimization and long-term legal stability.

ENGAGE, your strategic partner in Andorra

In an international environment where tax authorities cooperate closely, managing tax residency can no longer be approached as a mere administrative formality.

It is the keystone of our strategy, involving all aspects of wealth and tax structuring.

ENGAGE supports its customers with an integrated and rigorous approach, combining Andorran legal expertise, international taxation and a network of trusted partners.

This method secures each step of the process and ensures consistency between asset choices, economic situation, and declared tax residence.

By choosing Andorra as their wealth center of gravity, managers and investors benefit from a stable, predictable environment in line with international standards.

With ENGAGE, this implementation is based on a solid, documented and secure strategy.

3. Anticipate the risks of requalification and litigation

Against a backdrop of heightened surveillance of international flows, the French tax authorities now have extensive investigative resources at their disposal: automatic information exchange, monitoring of transfers, customs cooperation, and enhanced right of communication.

Cases of tax residence reclassification are on the rise, often as a result of poor planning or inconsistency in wealth management.

A simple inconsistency - residence declared in Andorra but main expenses or income received in France - can be enough to trigger proceedings.

The consequences are far-reaching:

- retroactive over several years,

- reminder of income tax and social security contributions,

- penalties of 40-80% for wilful default,

- even initiate proceedings for tax fraud.

ENGAGE implements a rigorous prevention methodology to avoid any drift:

- prior tax audit before transfer of residence,

- analysis of substance (actual activity, expenses, income, physical presence),

- a compliance file justifying actual residence,

- support in the event of a request for information or an accounting audit.

In the event of litigation, ENGAGE works hand in hand with its partner tax lawyers, both in Andorra and in France, to ensure a coherent, transnational defense. The aim is not simply to react to an audit, but to neutralize the risk before it arises.

4. Taxation, inheritance and family governance

Andorra's tax system is distinguished by its favorable approach to the transfer and preservation of family assets.

The total absence of inheritance and gift taxes creates an exceptional environment for families wishing to organize the intergenerational continuity of their assets.

ENGAGE helps its clients build sustainable family governance structures:

- transfer holdings, separating ownership and management;

- non-trading property companies (sociétés civiles immobilières - SCI) for holding property assets, with lower property taxes and flexible management;

- family charters setting out the rules of transmission, arbitration and distribution of power among heirs;

- dismemberment schemes (usufruct/ bare ownership) adapted to estate objectives.

In this context, taxation becomes a tool for stability and cohesion.

Wealthy families can retain control of family businesses while preparing for succession in a tax-neutral environment free from conflicts of interest.

Financial flows (dividends, income from securities, capital gains) can be optimized through holding structures or private investment funds, while respecting the economic substance required by Andorran legislation.

5. The strategic role of the integrated tax consultant

The success of a tax strategy depends not only on legal texts, but also on how they are interpreted and articulated.

In an environment where rules change every year, integrated tax advice becomes a governance lever that is as essential as financial or legal management.

ENGAGE performs this strategic function by bringing together complementary skills under one roof:

- tax specialists to ensure the legal security of operations,

- chartered accountants to control tax results and deductions,

- lawyers in corporate and international law,

- wealth advisors for estate planning,

- specialists in tax rulings to secure schemes with the authorities.

This coordination enables the development of robust strategies, where every decision—company formation, dividend transfers, land acquisitions, international investments—is anticipated from a tax perspective and documented.

The ENGAGE team also handles the annual follow-up of tax returns (income, company, property, VAT/IGI), manages advance payments and monitors legislative developments (new finance laws, European directives, tax treaties).

6. Ethical, sustainable and compliant taxation

The ENGAGE approach is based on three pillars: compliance, transparency and sustainable performance.

In a world where tax evasion and avoidance are severely punished, it's no longer a question of avoiding taxes, but of integrating them intelligently into your strategy.

A successful tax strategy is based on :

- the real economic substance of the structures created (offices, employees, bank accounts, measurable activity);

- traceability of financial flows, in compliance with the requirements of regulatory authorities;

- and complete documentation for each decision (deductions, depreciation, tax credits, tax exemption schemes).

ENGAGE rejects artificial arrangements and favors a long-term approach, in line with the Andorran philosophy of a simple but rigorous tax system.

This ethical vision appeals to managers and investors who want to combine economic efficiency with legal integrity.

In short, Andorra's tax system offers much more than just a numerical advantage: it provides a framework of stability for your assets and your business.

For business owners, it means being able to focus their efforts on growth, without the fear of constant tax changes.

For the investor, it's the assurance of a predictable net return and a smooth transfer of ownership.

For the family holding the assets, it is a model of continuity and peace of mind.

But the real advantage lies in the method: only a well-constructed, compliant and supported strategy can guarantee the success of an international tax project.

ENGAGE has made this its core business: transforming taxation into an instrument for performance, protection and transmission - with a single objective: the control and sustainability of your wealth.

III. Case study: an entrepreneur's journey

1. Entrepreneurial success in the face of tax pressure

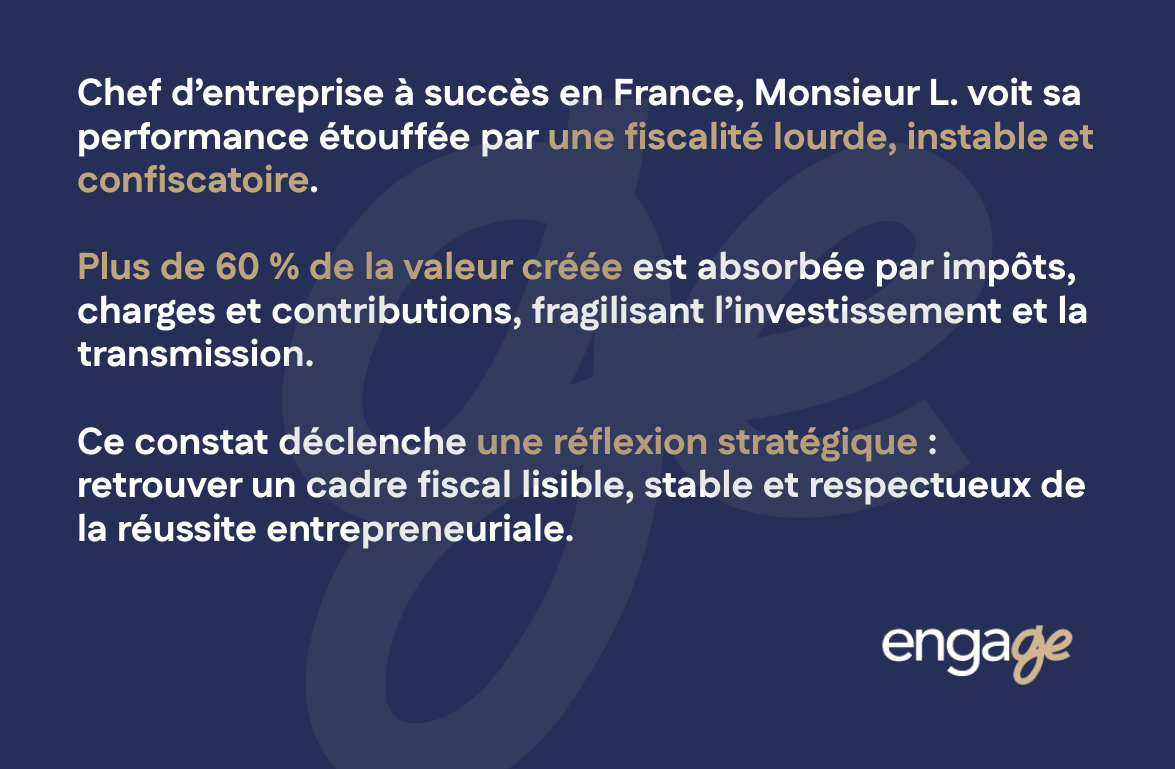

Mr. L., 52, is the epitome of a European entrepreneur: a visionary self-taught man who, in the space of twenty years, has gone from a 20 m² office to managing a digital services group present in five countries.

Based in France, his group employs 80 people and generates revenue of €12 million, with a portfolio of institutional and private clients.

But behind this success lies an increasingly burdensome reality: French taxation has become suffocating, legislative instability is chronic, and the administration is nitpicky, multiplying inspections and requests for supporting documents.

In 2022, his corporate income tax reaches 25%, his dividends are taxed at 30% (PFU), his personal income exceeds the 45% marginal bracket, and social security contributions add a further 17.2%.

Added to this are the CFE, CVAE, property tax, residual business tax and a host of sector-specific contributions.

Every year, more than 62% of the Group's consolidated income goes to taxes and social security charges.

For a manager like Mr L., this situation is no longer viable:

- real profitability is eroding,

- investments are deferred,

- and family inheritance becomes virtually impossible without immediate cash to pay inheritance tax.

Despite careful management and competent accounting firms, Mr L. has come up against a tax and regulatory wall.

Margins are melting, audits are multiplying, and a sense of injustice is setting in.

"I felt like I was working 100 hours an hour to finance a system that punished me for my success. It was no longer a business project, but an obstacle course."

Faced with this situation, he decided toembark on a strategic reflection: not to escape taxation, but to rediscover a stable, legible tax framework that respects the work accomplished.

It was with this in mind that he met ENGAGE, on the recommendation of a fellow manager who had already helped him set up in Andorra.

2. Diagnosis: unbalanced heritage architecture

The asset and tax audit conducted by ENGAGE quickly reveals a profound misalignment between the group's economic performance and its legal and tax structure.

The findings are clear:

- Multiple legal entities: four separate companies, created over time, each subject to a different tax regime, with no consolidated logic.

- Complex and costly financial flows: dividends, management fees, royalties, internal rents... subject to several levels of taxation and levies.

- Lack of a governance strategy: the family holding company has no shareholders' agreement or organized succession plan.

- Exposed real estate assets: directly owned by the executive, with no legal protection or property optimization.

- Inefficient remuneration: a high salary to compensate for deductions, reducing reinvestment capacity.

- Risk of reclassification: certain poorly documented intra-group transactions could be considered as profit transfers, exposing the group to tax adjustments. On a personal level, Mr. L. is resident in France for tax purposes, where he is subject to the progressive tax scale, the IFI (property wealth tax), social security contributions, and a disproportionate level of complexity in his tax returns.

In summary: Strong economic performance, significant assets, but an inconsistent tax and legal framework.

ENGAGE makes a simple observation: it's not the business that needs changing, but the architecture.

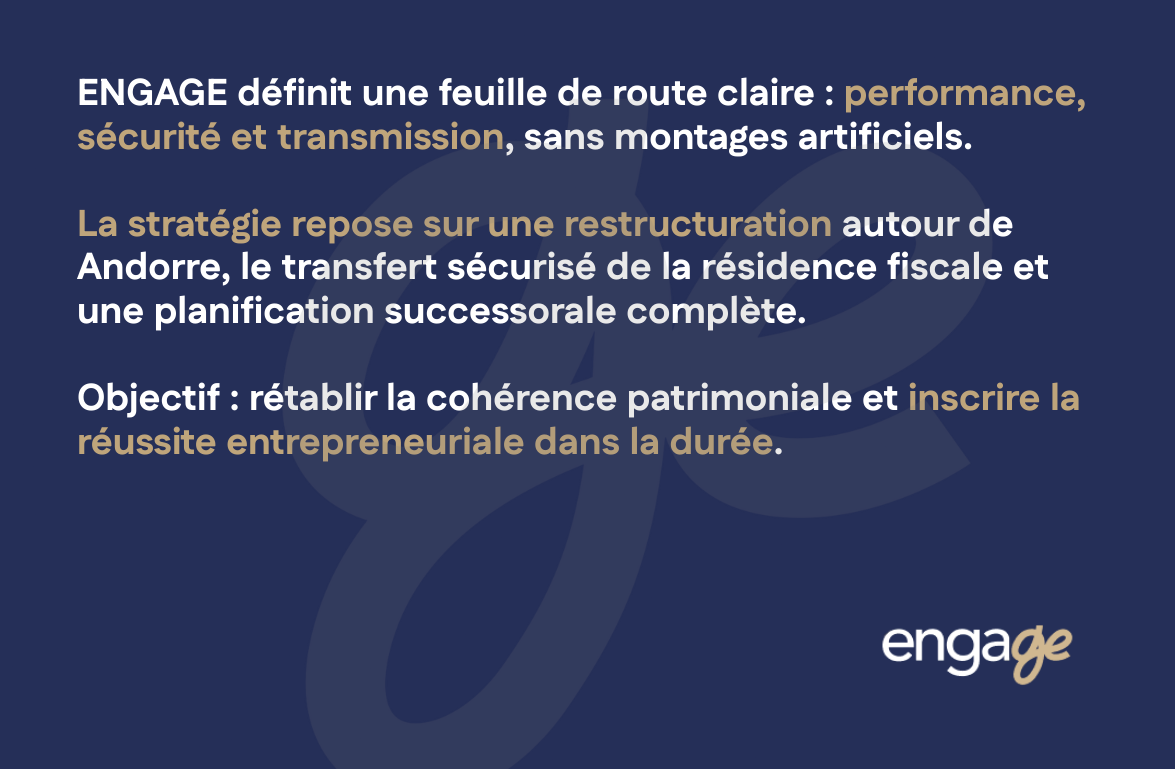

3. Objectives: performance, safety, transmission

During the strategic diagnosis, ENGAGE and Mr L. defined a three-pronged roadmap:

- Reduce overall tax pressure sustainably, without resorting to any artificial mechanism.

- Protect personal and business assets, by isolating risks and securing assets.

- Prepare the transfer of securities and assets to your children without any tax complications.

These objectives require a complete rebalancing of assets, in terms of legal aspects (creation of new structures), tax aspects (choice of residence and agreements), and asset management aspects (transfer, inheritance, governance).

ENGAGE proposes an integrated strategy based on three levers:

- restructuring the group around an andorran holding company;

- transfer of the manager's tax residence to Andorra, in accordance with legal criteria;

- comprehensive estate and wealth planning , supervised by accredited legal and tax experts.

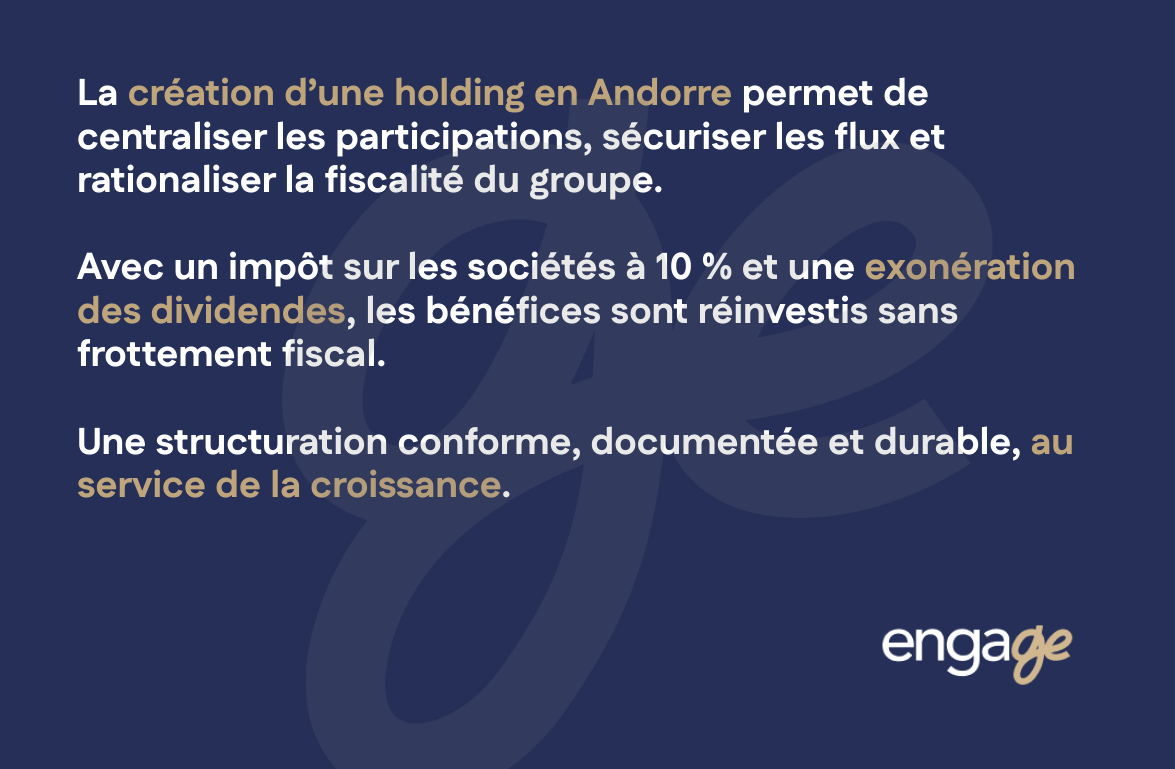

4. Group structure: the creation ofan Andorran holding company

ENGAGE recommends setting up an Andorran holding companyto become the group's parent company.

Its role is to centralize holdings, secure flows and rationalize the taxation of profits.

Device features :

- Legal form: Societat Limitada Unipersonal (SLU), equivalent to the French SARL.

- Purpose: to hold securities, manage financial assets and collect dividends.

- Taxation: corporate tax at 10%, total exemption on dividends received from subsidiaries, and full deductibility of management expenses.

The French operating companies remain in place and continue their local activities.

Flows are regularized and justified by service agreements that comply with the arm's length principle.

The transfer price is documented, margins are adjusted, and the economic substance of the holding company is demonstrated (premises, administrative staff, accounts, board of directors).

ENGAGE also ensures that the scheme complies with the provisions of the tax treaties between France and Andorra, thus avoiding any risk of double taxation.

As a result, the holding company receives dividends from its subsidiaries in a tax-optimized and perfectly compliant framework .

Profits can be reinvested in new projects without intermediate taxation.

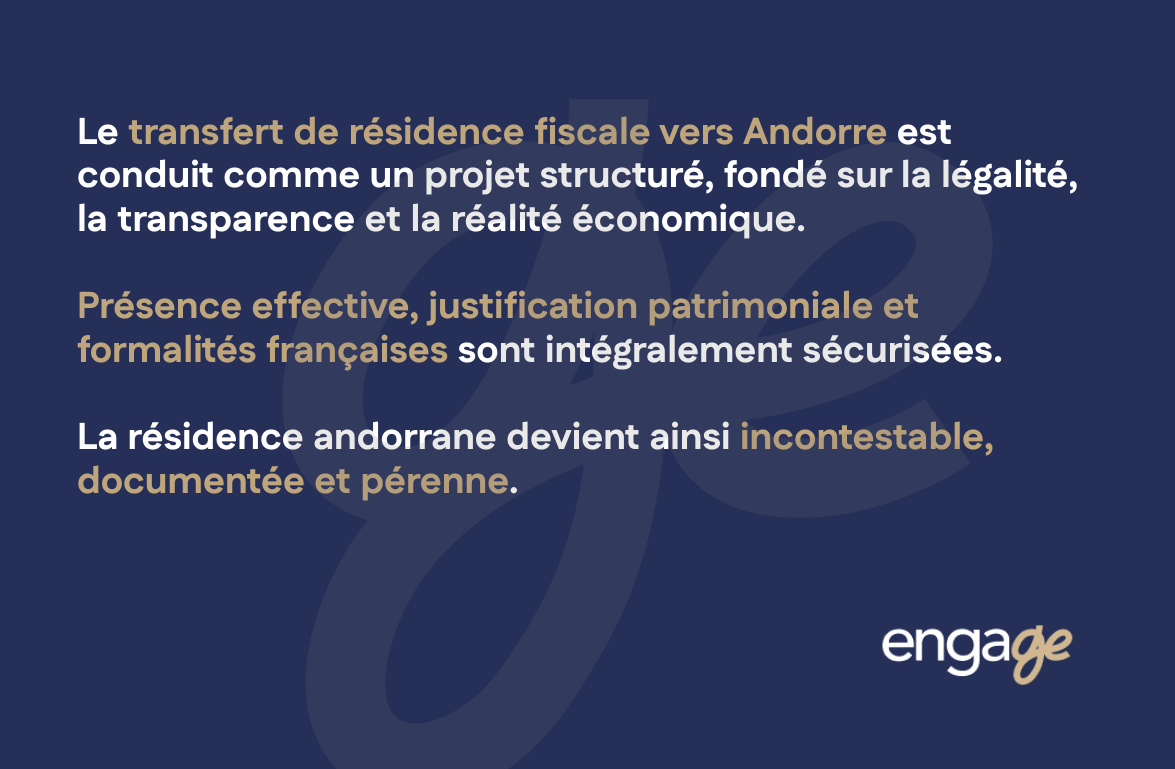

5. Transferring tax residence : a controlled change

The second step is to transfer Mr. L.'s tax residence to Andorra, not out of opportunism, but for reasons of economic and asset consistency.

ENGAGE oversees the process according to three principles: transparency, legality, and economic justification.

Transfer stages :

- Obtaining active resident status: Mr L. has a capital investment, a permanent home and full health cover.

- Proof of actual residence: presence in the area for more than 183 days a year, municipal registration, local subscription contracts, bank accounts, business relations.

- Notification to French authorities: filing of departure declaration, deregistration formalities, transmission of form 2042-NR, tax return for year of departure.

- Verification of the scope of application of the exit tax.

- ENGAGE demonstrates that the shares have been held for more than two years and that the transfer is based on a genuine economic reason.

The tax residence file, meticulously prepared, includes more than 200 supporting documents: contracts, invoices, administrative correspondence, and notarized certificates.

This substance file is the best guarantee in the event of an inspection or request for information.

It proves that Mr. L.'s Andorran tax residence is not fictitious but fully justified and legitimate.

6. Estate planning: tax-free inheritance

ENGAGE then assists Mr. L. in drafting a family transfer agreement based on the stability of the Andorran framework.

The strategy is based on the creation of a family charter, validated by an Andorran jurist and a French notary, defining :

- Group governance rules,

- the distribution of shares,

- voting rights and dividends,

- pre-emption and inalienability clauses.

Thanks to the absence of inheritance and gift taxes in Andorra, Mr L. is gradually passing on the holding company's shares to his children at no tax cost.

French real estate assets, now held via Andorran property companies, are also exempt from the IFI and benefit from an advantageous depreciation regime.

ENGAGE ensures that each transfer is documented, registered and notified, guaranteeing recognition of the system by the authorities.

This transparency avoids any suspicion of tax evasion or fictitious activities.

7. Operational implementation: coordination and control

During the 24 months of implementation, ENGAGE acts as a fiscal and legal conductor:

- coordination between tax specialists, notaries, chartered accountants and bankers,

- drafting of intra-group agreements,

- registration and declaration follow-up,

- supervision of accounting entries,

- preparation of consolidated tax returns,

- and annual compliance verification.

It summarizes financial flows, dividends paid, expenses charged and deductions made, guaranteeing full traceability of the strategy.

This rigor, based on documentation and economic consistency, is the key to the legal durability of the package.

8. Results: performance, safety and peace of mind

After three complete exercises, the effects are measurable and long-lasting:

- Overall tax rate (corporate income tax + personal income tax) reduced from 62% to 15%.

- Consolidated net margin up 48%.

- Isolated, legally protected real estate .

- Transfer of shares free of inheritance tax and other taxes.

- No disputes, no adjustments, no cross-checking.

Andorra's regulatory stability enables Mr. L. tomake five-year forecasts with a degree of precision unknown in France.

Its assets are now structured, transferable and compliant.

9. The human factor: reconciliation with taxation

One of the most significant effects, beyond the numbers, is psychological.

Mr L. no longer refers to taxation as a threat, but as a steering parameter.

He found what every entrepreneur seeks: the freedom to act with clarity.

"Taxation is no longer an obstacle to my decisions.

It has become a framework that I understand, that I master, and in which I move forward serenely."

ENGAGE often stresses this point: peace of mind is an intangible asset, just as precious as financial returns.

A tax-compliant manager is a more creative, daring and sustainable manager.

10. Lessons learned: a reproducible, controlled strategy

This case highlights a simple truth: the success of tax optimization relies less on the search for a low rate than on the quality of the method.

ENGAGE systematically applies three founding principles:

- Economic coherence: each structure must respond to a real business logic.

- Complete documentation: every flow, every transfer, every agreement must be justified and recorded.

- International transparency: everything must be able to be presented to the tax authorities, without ambiguity or artifice.

It is this need for coherence that transforms a tax advantage into a legitimate and sustainable wealth strategy.

11. The ENGAGE philosophy: the ethics of planning

ENGAGE stands out with a clear vision :

"Tax optimization isn't an escape, it's an organization."

Its approach is based on compliance, method and transparency.

The firm's experts - tax specialists, lawyers and chartered accountants - work together to build robust, compliant and documented solutions, in perfect cooperation with local authorities.

Far from tax avoidance or artificial domiciliation practices, ENGAGE promotes reasoned taxation, where performance is based on clarity, rigor and compliance.

Today, this ethic is a mark of confidence : it reassures banks, partners, investors... and the tax authorities themselves.

12. Case study conclusion: taxation as a lever for wealth sovereignty

Three years after its reorganization, Mr. L. is the embodiment of the success story of controlled taxation.

His group is more profitable, his family protected, and his assets transferable.

But above all, it has regained sovereignty over its fiscal destiny.

Andorra has not been a refuge, but a rational and secure setting, where taxation rewards investment and transparency.

ENGAGE, through its structured approach and its commitment to compliance, has enabled its client to rebuild a coherent, legally-compliant estate, geared to the transfer of assets.

"Wealth success is measured not just in tax rates, but in stability, security and freedom of action."

ENGAGE has made this its credo: to transform taxation into an instrument of confidence and sovereignty, at the service of your assets, your business and your legacy.

IV. The ENGAGE process: a 7-step method for structuring, securing and optimizing your tax situation

At ENGAGE, taxation is not an adjustment variable: it's a strategic lever.

The firm's mission is to transform complex tax situations - often undergone or poorly coordinated - into coherent, stable and compliant asset architectures.

To achieve this result, ENGAGE has designed an exclusive seven-step methodology based on three cardinal principles:

- Absolute compliance with national and international tax laws,

- Consistency between economic activity, residence and financial flows,

- Full traceability of every decision, to guarantee the legitimacy of the system in the event of an audit.

This structured approach enables all business owners, investors and wealthy families to regain control of their tax affairs and build a sustainable, legal and effective wealth strategy.

Step 1: The wealth and tax audit - analyze to understand

It all starts with a complete audit, a true radiography of the customer's assets.

This phase aims to identify optimization levers and areas of vulnerability.

ENGAGE collection and analysis :

- professional and property income,

- Group structure (companies, holdings, SCI, foncières, etc.),

- past and current tax returns,

- real estate and personal property (portfolios, assets, debts, unrealized capital gains),

- the tax residence of the client and their family,

- life and transmission objectives (sale, retirement, expatriation, succession).

This audit takes place in absolute confidentiality, following a secure procedure that complies with the RGPD.

The ENGAGE team then evaluates:

- the level of effective tax pressure,

- consistency between declared residence and economic reality,

- deductibility of expenses,

- the legal and accounting structure of the assets,

- and the risks of requalification or abuse of rights.

At the end of this first stage, the customer receives a wealth and tax situation report: a clear, factual and quantified document, highlighting areas for improvement and legal opportunities.

"The audit is the starting point of any strategy: before optimizing, you have to understand."

Step 2: Strategic diagnosis - defining objectives and scenarios

The audit is the first step in the process, but the strategy is born out of the overall diagnosis of the company's assets.

ENGAGE translates the data collected into a strategic vision based on the customer's needs:

- Reducing the tax burden,

- Protection of personal assets,

- Estate planning,

- Preserving confidentiality,

- Stable legal and tax framework,

- Preparing a change of residence,

- or international business development.

This stage consists of bringing the existing situation into line with long-term objectives: should we create a holding company, merge structures, dissociate activities, outsource intellectual property, set up a real estate company, or simply reorganize flows?

ENGAGE presents the customer with several comparative scenarios, illustrated by concrete simulations:

- tax cost before/after restructuring,

- impact on revenues, dividends and profits,

- effects on cash flow and transmission,

- legal compliance according to the jurisdictions concerned.

This diagnostic phase leads to a detailed asset roadmap, setting out the target strategy and implementation milestones.

Stage 3: Designing the legal and tax framework - structuring for protection

Once the strategy has been defined, ENGAGE designs the optimum legal and tax structure.

This stage mobilizes the firm's cross-disciplinary skills: tax specialists, chartered accountants, corporate lawyers, wealth advisors and partner notaries.

Each diagram is built according to a three-dimensional logic:

- Economic - the structure must reflect the real business (substance, workforce, sales flows, customers).

- Legal - it must protect assets and enable stable governance (shareholders' agreements, articles of association, pre-emption clauses, differentiated voting rights).

- Tax - to optimize the overall cost within a compliant framework (reduced rates, deductibility, exemptions, tax credits).

The most common devices include :

- setting up an Andorran holding company (10% corporation tax, exemption on dividends received);

- setting upa property or asset management company (deduction of expenses, depreciation);

- the creation of a family transmission vehicle (differentiated shares, dismemberment, tax-free donation);

- structuring the provision of services between entities to reflect the reality of economic flows.

Each step is documented, validated by a tax and legal memo and, if necessary, subject to prior rescript with the relevant authorities.

Step 4: Compliance validation - secure before you execute

ENGAGE's strength lies in its ability to validate upstream the conformity of each structure.

This stage consists of securing the legal and tax aspects of the system before any operational implementation.

Teams write :

- an international tax compliance report,

- a legal note of economic substance,

- a transfer pricing documentation file,

- and, where applicable, a file on tax residence.

These documents serve to demonstrate the economic coherence of the package and prevent any risk of subsequent litigation.

They may be produced in the event of an accounting audit, a request for information or an exchange of information.

"What makes a strategy unassailable is documentation and consistency."

Stage 5: Operational implementation - coordinating and executing

Once compliance has been validated, ENGAGE orchestrates the operational implementation of the system.

This phase is crucial: it's the transition from concept to economic reality.

It involves coordinating an ecosystem of experts:

- lawyers specializing in company law and notaries for incorporation and amendments to articles of association,

- accountants for recording entries,

- bankers to open accounts and set up flows,

- insurers and asset protection managers,

- lawyers for intra-group contracts and governance pacts.

ENGAGE acts as a tax orchestra conductor, guaranteeing alignment between stakeholders and consistency of flows:

- service agreements,

- inter-company billing,

- dividend payments,

- expense allocations,

- amortization and provisions,

- allocation of taxable income.

Step 6: Control and reporting - measuring, adjusting, documenting

A tax strategy is only as good as its monitoring and updating.

ENGAGE ensures regular reporting and implements an annual control system.

Objectives:

- check compliance of declarations and payments,

- adjust strategy in line with new finance laws,

- integrate changes in the customer's situation (income, assets, inheritance, residence),

- and maintain an impeccable level of documentation.

Each year, ENGAGE produces a tax and asset balance sheet, including :

- a consolidated tax report,

- a summary of intra-group flows,

- a compliance audit of declared operations,

- update recommendations (e.g. new exemptions, tax credits, applicable regimes).

This reporting, comparable to that of an in-house tax department, ensures long-term stability and maximum responsiveness to changes in the law.

Step 7: Asset management and succession planning - sustaining and anticipating the future

Last but not least, ENGAGE supports its customers over the long term.

Taxation is not a one-off project: it is a dynamic area of responsibility that must adapt to changes in laws, markets, and families.

Follow-up includes :

- updating company bylaws,

- estate planning (donations, dismemberments, family charters),

- revision of intra-group contracts,

- simulation of tax impacts in the event of sale or inheritance,

- and coordination with the customer's financial and notary advisors.

Customers are no longer content to simply benefit from a tax advantage: they become the protagonists of a living wealth strategy, aligned with their economic and family objectives.

A proven method: rigor, transparency and performance

The ENGAGE method stands out for its traceability, compliance and strategic added value.

It doesn't promise the impossible: it guarantees reliability, legality and sustainability.

By combining Franco-Andorran tax expertise, accounting precision and wealth management vision, ENGAGE offers each customer a comprehensive, sustainable and well-documented solution.

In a nutshell:

- The audit provides the vision,

- The diagnosis defines the strategy,

- Structure creates coherence,

- Validation guarantees compliance,

- Putting it into practice,

- Control makes it last,

- And the follow-up ensures the transmission.

Conclusion - The ENGAGE method, a signature of reliability

In a world where taxation has become an issue of competitiveness and sovereignty, the ENGAGE method embodies a balanced approach: that of legal, assertive and transparent optimization.

Each step aims to restore what tax complexity has often led to: clarity, control and confidence.

Thanks to this method, managers, investors and wealthy families can build a long-term strategy based on :

- the stability of the Andorran framework,

- legal certainty for structures,

- and measurable asset management performance.

ENGAGE doesn't just assist with a tax transfer: it designs, secures and implements a complete wealth management project, with absolute respect for the law and international transparency.

V. The ENGAGE vision of international taxation: rigor, consistency and collective intelligence

1. Rethinking taxation in a changing world

Over the past decade, international taxation has undergone a profound transformation.

The days of "opaque territories" and artificial arrangements are a thing of the past.

Under the impetus of the G20 and the OECD, automatic exchanges of information, the BEPS(Base Erosion and Profit Shifting) rules, banking transparency and the digital traceability of flows have redefined the global tax landscape.

This change requires business leaders, investors, and wealthy families to rethink their relationship with taxation: no longer as a constraint to be circumvented, but as a strategic factor to be managed.

"Taxation is no longer a field of avoidance. It's a language of compliance, sovereignty and projection."

In this new paradigm, Andorra has established itself as a model: a modern, transparent state, aligned with European standards, but offering stable, proportionate taxation that respects real economic activity.

It is precisely in this balance that ENGAGE anchors its expertise: designing sustainable, compliant and intelligent tax strategies, at the crossroads of law, wealth management and governance.

2. The intellectual foundations of the ENGAGE approach

At ENGAGE, each tax consultancy is based on a clear and assertive intellectual architecture, structured around three guiding principles:

compliance, consistency and predictability.

a) Compliance - the cornerstone of tax security

Compliance is the sine qua non of stable, defensible taxation.

It's not just a matter of complying with declarations or filing tax returns: it implies total traceability of decisions, flows and economic justifications.

A compliant strategy means :

- real economic substance (offices, employees, contracts, governance),

- justified cash flows, invoiced at fair market value,

- comprehensive documentation, ready to be produced at any time,

- and, if necessary, prior validation by the administration ( tax ruling, certificate, approval).

Conformity protects the taxpayer against misinterpretation.

It creates a relationship of trust between the administration and the company.

And, above all, it gives clients peace of mind knowing that their wealth management strategy is based on a solid foundation.

"The taxpayer who documents, demonstrates and declares correctly is never afraid of an audit. Compliance is our first form of protection."

b) Coherence - the intelligence of the structure

A healthy tax system is first and foremost a coherent one.

Coherence is the art of aligning the legal, tax and asset aspects of a project.

In other words: ensure that the form and content tell the same story.

ENGAGE ensures that each strategy is coherent on three levels:

- Legal consistency: the structure(holding company, property company, non-trading company, etc.) must correspond to a real activity and an identifiable objective.

- Tax consistency: the location of income and expenses must reflect the place where value is created.

- Heritage consistency: assets, governance, and transfer must be considered in the same way as the business itself.

An Andorran company without substance, a holding company without shareholdings, or a tax residence without an effective presence are all vulnerabilities.

ENGAGE builds logical, vibrant, and legitimate structures where every decision makes sense.

"Consistency is what transforms an arrangement into a strategy. It is also what distinguishes tax engineering from mere opportunism."

c) Predictability - the key to asset confidence

Wealthy entrepreneurs and investors are not afraid of taxes: they fear unpredictability, sudden reforms and changes in doctrine.

Andorra stands out precisely for this stability.

Its tax system is based on a constant foundation, framed by law and protected from political instability.

The rates are known, stable and do not change with each budget:

- 10% on companies,

- 10% on income,

- 0% on inheritances and gifts,

- exemption on capital gains and certain foreign income.

This predictability makes it possible to plan for twenty years, not two.

ENGAGE transforms this stability into an intergenerational strategy: each structure designed today is designed to withstand both economic cycles and political changes.

"The real tax luxury isn't the rate: it's visibility."

3. Collective intelligence: the strength of a cross-functional board

Taxation is a language shared by several disciplines: law, accounting, management, finance, strategy and succession.

ENGAGE therefore approaches it not as an isolated field, but as an interconnected system.

Its model is based on organized collective intelligence, where each expert contributes a building block to the overall structure:

The tax expert

It analyzes, structures and secures. It ensures compliance with international conventions and OECD guidelines.

He determines the applicable rates, the possible deductions and the optimal declaration strategy.

The lawyer

He translates the customer's vision into legal structures.

He drafts articles of association, shareholders' agreements, intra-group agreements and management contracts.

Its role is to make the system legally invulnerable.

The chartered accountant

He is the guardian of the tax result.

It verifies the economic reality of flows, the deductibility of expenses, and the consistency of balance sheets between jurisdictions.

It ensures that strategic decisions are properly accounted for.

The wealth advisor

It ensures continuity: it is the link between taxation, wealth and family.

Its role is to integrate the human dimension - succession, inheritance, life insurance, retirement - into a global planning approach.

The banker and the partner auditor

They complete the system: financing, investment, anti-money laundering compliance, CRS reporting.

This multidisciplinary approach helps to avoid "grey areas" where tax decisions are no longer aligned with legal or accounting logic.

At ENGAGE, no structure lives in isolation: everything functions as a coherent, living, auditable organism.

4. Technical Box - Seven mistakes to avoid in international planning

ENGAGE regularly identifies recurring mistakes made by managers or investors who have tried to structure their tax affairs without comprehensive support.

These mistakes, often made in good faith, can have serious consequences.

1. Confusing administrative residence with tax residence

Tax residence does not depend on a postal address, but on the center of economic and family interests.

A customer who declares that he lives in Andorra but keeps his business, accounts and family in France is liable to requalification.

2. Creating structures without substance

A company with no offices, no real activity and no staff is considered fictitious.

The tax authorities may reclassify it as a permanent establishment and tax all its income.

3. Neglecting flow documentation

Service, management and license agreements must be drawn up, updated and justified.

In the event of an inspection, the absence of documents is sufficient to reverse the burden of proof.

4. Forget accounting harmonization between countries

A flow declared as a charge in France must appear as a product in Andorra.

Bilateral inconsistencies are the primary trigger for transfer pricing controls.

5. Ignore inheritance tax

A scheme that is tax-efficient in the short term can be disastrous if it does not take into account the question of succession (inheritance tax, family governance, dismemberment).

6. Underestimating the scope of banking transparency

Since the implementation of the CRS standard, all banks automatically exchange information on accounts, dividends and capital gains.

Anonymity no longer exists: only proactive transparency protects.

7. Choose a standardized solution

The "turnkey" models offered on the Internet are often unsuitable.

Each situation must be personalized, contextualized and validated.

When it comes to taxation, copying and pasting is the biggest risk of all.

5. Andorra, a balanced and responsible tax system

Andorra is no longer defined by its low rates, but by the coherence of its system.

It's a tax model that rewards compliance and stability, not opacity.

ENGAGE sees it as a testing ground for a new form of taxation:

- a simple, clear, single-rate tax,

- a pragmatic administration, open to dialogue,

- full transparency vis-à-vis the OECD,

- a liberal and predictable wealth tax system.

Far from the logic of unfair competition, Andorra embodies a balanced approach to taxation, where legitimacy is based on proportionality: those who create, invest and employ are rewarded with stability and clarity.

"Andorra is to taxation what neutrality is to diplomacy: a posture of respect, balance and predictability."

6. A doctrine for action: taxation as sovereignty

ENGAGE defends a strong idea: regaining control of your taxes means regaining control of your assets.

When understood and anticipated, taxation becomes a tool for individual and entrepreneurial sovereignty.

This doctrine is based on twelve fundamental convictions:

- Anticipate rather than suffer

- Tax laws evolve, but a well-designed system remains defensible.

- Anticipation - audit, diagnosis, documentation - is more effective than reaction.

- Declare rather than conceal

- Transparency is not a weakness: it's a strategy.

- A taxpayer who correctly declares and justifies his flows retains control of the dialogue with the tax authorities.

- Document rather than assume

- An undocumented transaction loses all probative value.

- ENGAGE makes traceability a cardinal principle: everything must be able to be demonstrated, explained and archived.

- Structuring for transmission

- Taxation doesn't stop at income tax: it encompasses governance, transmission and succession.

- A successful structure is one that outlives its founder.

"The real success of a tax strategy is that it continues to produce its effects without its creator."

7. ENGAGE, a global consulting model

ENGAGE does not see itself as a mere tax consultancy.

We are an international wealth engineering firm at the crossroads of law, tax and strategy.

Its role: to transform tax complexity into a lever for growth, protection and transmission.

Each mission is carried out according to a project governance logic:

- a single file manager,

- cross-functional coordination between experts,

- validation at every stage (legal, accounting, tax, asset management),

- clear, structured reporting to the customer.

ENGAGE doesn't sell fixtures: it builds architectures.

Each case is unique, each strategy argued, each result documented.

This requirement explains why ENGAGE is now recognized as a key player in Franco-Andorran tax planning.

8. In summary - Taxation as the art of coherence

In a world where information circulates, tax borders are disappearing and compliance is becoming universal, competitive advantage no longer lies in secrecy, but in consistency and control.

ENGAGE has made this its signature:

- The rigor of numbers,

- Clear structures,

- Transparent processes,

- Stability over time.

"Taxation shouldn't be a risk, it should be a controlled language. ENGAGE is the clearest translation of this."

VII. Conclusion - Anticipating, structuring, transmitting

1. Taxation as a mirror of strategy

In a world where the mobility of capital, talent and companies has become the rule, taxation is no longer simply a legal framework:

it has become the mirror of strategy.

Every economic decision, every investment, every transmission reveals its coherence - or its flaws.

Gone are the days when you could delegate your tax affairs entirely to intermediaries without understanding the logic behind it.

Today's enlightened manager or investor needs to think fiscally, i.e. integrate taxation into his or her strategic, wealth and inheritance planning.

ENGAGE is part of this new approach: giving taxpayers back the power to understand and manage their tax affairs.

"When controlled, taxation becomes a tool of sovereignty."

2. From constraint to control

For a long time, taxation was perceived as an external constraint, imposed or imposed upon us.

This perception is fuelled by the growing complexity of tax scales, the multiplication of levies and the volatility of finance laws.

But there's another way of looking at it: that of mastery.

Taxation can be planned, organized and balanced within a fully compliant and transparent framework.

ENGAGE transforms this constraint into an opportunity:

- by revealing the legal levers of tax reduction,

- documenting each decision,

- and by integrating tax aspects into the overall wealth strategy.

It is in this transition - from constraint to control - that the difference lies between being taxed and managing one's tax environment.

3. Andorra: stability, transparency, security

The Principality of Andorra stands out as a rare model of fiscal balance.

Between France and Spain, it offers a credible and responsible alternative:

- Regulatory stability: tax laws change little and are clear.

- Moderate rates: 10% corporate tax, 10% income tax.

- No inheritance or gift tax.

- Simplified VAT system (IGI): 4.5% at standard rate.

- International compliance: full adherence to OECD and BEPS standards.

Added to this are a secure living environment, a solid banking system and an administration open to dialogue.

It's not a "refuge", but a space of predictability and legitimacy.

This is the consistency that ENGAGE offers its customers:

not run away, but choose a sustainable and rational model, both fiscal and legal.

"Andorra is not a way out. It's a projection towards a balanced and respected tax system."

4. ENGAGE's role: transforming complexity into clarity

Tax rules, international conventions and case law form a dense, shifting and sometimes confusing universe.

ENGAGE's role is to translate this complexity into clear, structured and defensible solutions.

Each case begins with a careful listening session to understand the situation, the objectives, the sensitivity to risk and the family's ambitions.

Then comes the audit, the mapping, the construction of a customized tax and wealth scenario.

The firm's experts work in synergy:

- the tax expert secures the legal foundations,

- the lawyer supervises acts and contracts,

- the chartered accountant ensures accounting consistency and traceability,

- the wealth advisor integrates the human and inheritance dimension.

The result is a living, coherent and sustainable tax architecture.

ENGAGE does not sell fixtures:

it designs strategies - legitimate, rational and documented.

5. Compliance as added value

In the ENGAGE vision, compliance is not a hindrance: it's a competitive advantage.

A clear, traceable and compliant structure inspires confidence in banks, investors, heirs and authorities.

The firm draws up a proactive compliance file for each customer, which is updated every year and includes :

- justification of the center of economic interests,

- proof of actual residence,

- documentation of flows and services,

- consistency between the balance sheets of different jurisdictions.

This documentary discipline transforms the tax audit into an argumentative dialogue.

The customer is no longer in a defensive position: he demonstrates, he proves, he masters.

"In a transparent tax world, compliance is no longer an option: it's an assurance."

6. Structuring for transmission

Taxation only makes sense if it is part of an intergenerational logic.

Optimizing the present without thinking about the future means creating long-term fragility.

ENGAGE systematically integrates the succession dimension into the design of each scheme:

- transmission pacts,

- adapted dismemberments,

- family companies,

- heritage governance,

- provident and insurance schemes.

The goal: a smooth, tax-free and conflict-free inheritance.

Thanks to the absence of inheritance and gift taxes, Andorran structures preserve the integrity of family assets, while maintaining transparency and governance.

"A successful transmission is one that creates neither inequality nor litigation.

7. ENGAGE ethics: the exact opposite of evasion

ENGAGE stands out for its uncompromising ethics:

no artificial set-ups, no front companies, no optimization disconnected from reality.

The firm's approach is based on three ethical principles:

- Legality: any scheme must be defensible before a tax authority.

- Transparency: everything must be explained, proven and justified.

- Substance: any structure must be based on activity, real flows and tangible governance.

This rigor, far from restricting performance, reinforces it.

A transparent structure inspires the confidence of banking partners and reassures tax authorities.

ENGAGE has chosen a clear path: that of compliant performance.

"Transparency is no longer the enemy of optimization. It has become its condition.

8. Taxation and wealth sovereignty

Globalization has standardized rules, but it has also created a new requirement: that of individual sovereignty.

In this context, tax management is not a question of selfishness, but of responsibility.

A well thought-out tax system makes it possible to :

- protect its heritage,

- secure your retirement,

- anticipate transmission,

- and free up resources to invest, create and undertake.

ENGAGE stands for this simple idea:

controlled taxation is an instrument of economic freedom.

It allows the entrepreneur to focus on value creation, the family on continuity, and the investor on projection.

9. Anticipating, structuring, passing on: the triptych of tax peace of mind

- Anticipate: because taxation rewards preparation, not improvisation.

- Structure: because legal clarity protects you better than the lowest rate.

- Passing on: because an estate is only meaningful if it lasts over time.

ENGAGE embodies this triptych:

anticipating reforms, structuring wealth, passing on success.

Every customer becomes a player in his or her own tax affairs, rather than a spectator.

Each strategy becomes a framework for stability, rather than a risk zone.

"Anticipating, structuring and passing on: that's the essence of wealth management.

10. Taxation, a language of trust

The aesthetics of taxation are well thought out.

When it is balanced, coherent and compliant, it becomes a language of trust between citizens, companies and the State.

Andorra is an example of this: a simple, clear and stable system, where the administration accompanies rather than punishes.

This is the philosophy that ENGAGE stands for:

restore trust between wealth and law, between success and compliance.

"Taxation shouldn't punish success; it should frame it intelligently."

11. In conclusion: choose clarity

Choosing ENGAGE means choosing clarity.

It means rejecting opaque solutions, easy promises and risky schemes.

It means preferring structure, method and conformity, in the service of sustainable performance.

Andorra's tax system, overseen by expert advice, is a real lever for stability.

It offers entrepreneurs and investors the opportunity to regain control of their tax situation, their assets and their future.

12. Call to action

If you are a manager or an investor, or if you want to prepare for the transfer of your company within a legal and secure framework, we can help.

- Contact ENGAGE for a complete and confidential asset audit.

- Click here to book a strategic meeting with a Franco-Andorran tax consultant.

- Discuss your project with a tax expert and discover how to transform your tax system into a tool for sovereignty.

ENGAGE, your partner for tax, asset and legal stability. Because a well-structured estate is the best form of freedom.